Audited financial statements for NLB d.d. and the NLB Group

Notes to the financial statements

Notes to the financial statements

1. GENERAL INFORMATION

Nova Ljubljanska banka d.d. Ljubljana (hereinafter: NLB) is a joint stock entity providing universal banking services. The NLB Group operates in more than thirteen countries.

NLB is incorporated and domiciled in Slovenia. The address of its registered office is Trg Republike 2, Ljubljana. NLB’s shares are not listed on the stock exchange.

NLB’s largest shareholders as at December 31, 2011 are the Republic of Slovenia, owning 45.62% of shares (December 31, 2010: 33.10%), and KBC Bank N.V. Brussels, owning 25.00% of shares (December 31, 2010: 30.57%). By increasing the capital of NLB, the Republic of Slovenia and its controlled companies exceeded 50% ownership in NLB. Republic of Slovenia together with its related companies presents the ultimate controlling party of NLB.

All amounts in the financial statements and in the notes to the financial statements are expressed in thousands of euros unless otherwise stated.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The principal accounting policies adopted for the preparation of the separate and consolidated financial statements are set out below. Policies have been consistently applied to all the years presented.

2.1. Statement of compliance

The principal accounting policies applied in the preparation of the separate and consolidated financial statements have been prepared in accordance with the International Financial Accounting Standards (hereinafter: the IFRS) as adopted by the European Union (hereinafter: EU). Additional requirements under the national legislation are included where appropriate.

The separate and consolidated financial statements comprise the income statement and statement of comprehensive income, the statement of financial position, the statement of changes in equity, the statement of cash flows, significant accounting policies and the notes.

2.2. Basis of presentation of financial statements

The financial statements have been prepared under the historical cost convention as modified by the revaluation of available for sale financial assets and financial assets and financial liabilities at fair value through profit or loss, including all derivative contracts, and investment property.

The preparation of financial statements pursuant to the IFRS requires the use of estimates and assumptions that affect the reported amounts of assets and liabilities and the disclosure of contingent assets and liabilities at the date of the financial statements, and the reported amounts of revenue and expenses during the reporting period. Although these estimates are based on management’s best knowledge of current events and activities, actual results may ultimately differ from those estimates. Accounting estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognized in the period in which the estimate is revised. Critical accounting policies and estimates are disclosed in note 2.31.

2.3. Comparative amounts

Except when a standard or an interpretation permits or requires otherwise, all amounts are reported or disclosed with comparative amounts. Where IAS 8 applies, comparative figures have been adjusted to conform to changes in presentation in the current year.

2.4. Consolidation

In the consolidated financial statements subsidiary undertakings, which are those entities in which the NLB Group, directly or indirectly, has an interest of more than one half of the voting rights or otherwise has the power to exercise control over operations, have been fully consolidated. Subsidiaries are consolidated from the date on which effective control is transferred to the NLB Group and are no longer consolidated from the date that control ceases. Where necessary, the accounting policies of subsidiaries have been amended to ensure consistency with the policies adopted by the NLB Group. The financial statements of consolidated subsidiaries were prepared as of the parent entity’s reporting date. Non-controlling interests are disclosed in the consolidated statement of changes in equity. Non-controlling interest is that part of the net results and of the equity of a subsidiary attributable to interests which are not owned, directly or indirectly, by NLB. The NLB Group measures non-controlling interest on a transaction by transaction basis, either at fair value, or the non-controlling interest's proportionate share of net assets of the acquiree.

Inter-company transactions, balances and unrealized gains on transactions between NLB Group entities are eliminated. Unrealized losses are also eliminated unless the transaction provides evidence of impairment of the asset transferred.

The NLB Group treats transactions with noncontrolling interests as transactions with equity owners of the NLB Group. For purchases from non-controlling interests, the difference between any consideration paid and the relevant share acquired of the carrying value of net assets of the subsidiary is deducted from equity. Gains or losses on sales to non-controlling interests are also recorded in equity. For sales to noncontrolling interests, the differences between any proceeds received and the relevant share of noncontrolling interests are also recorded in equity.

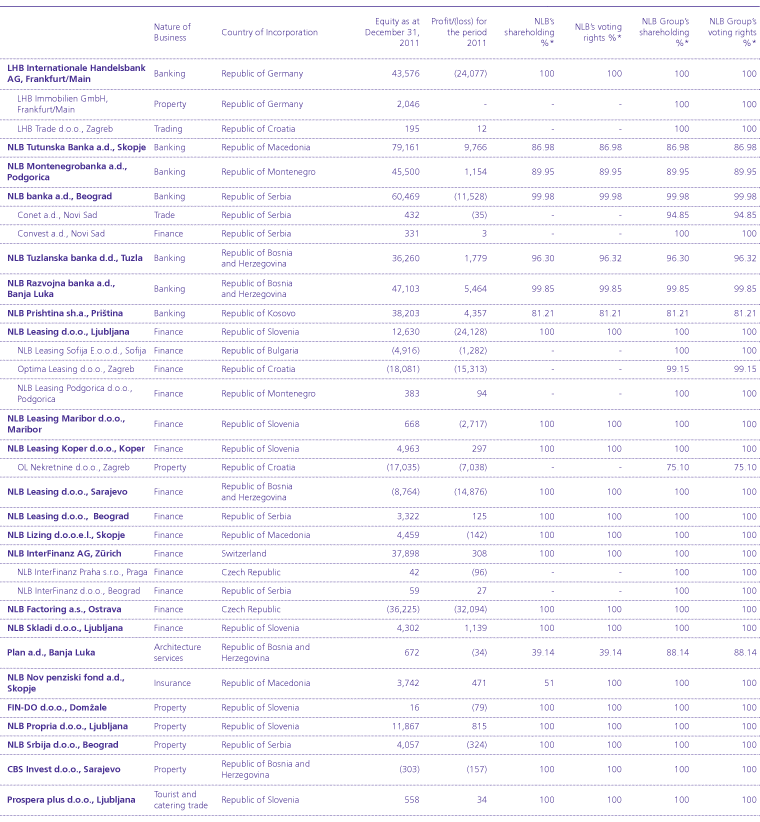

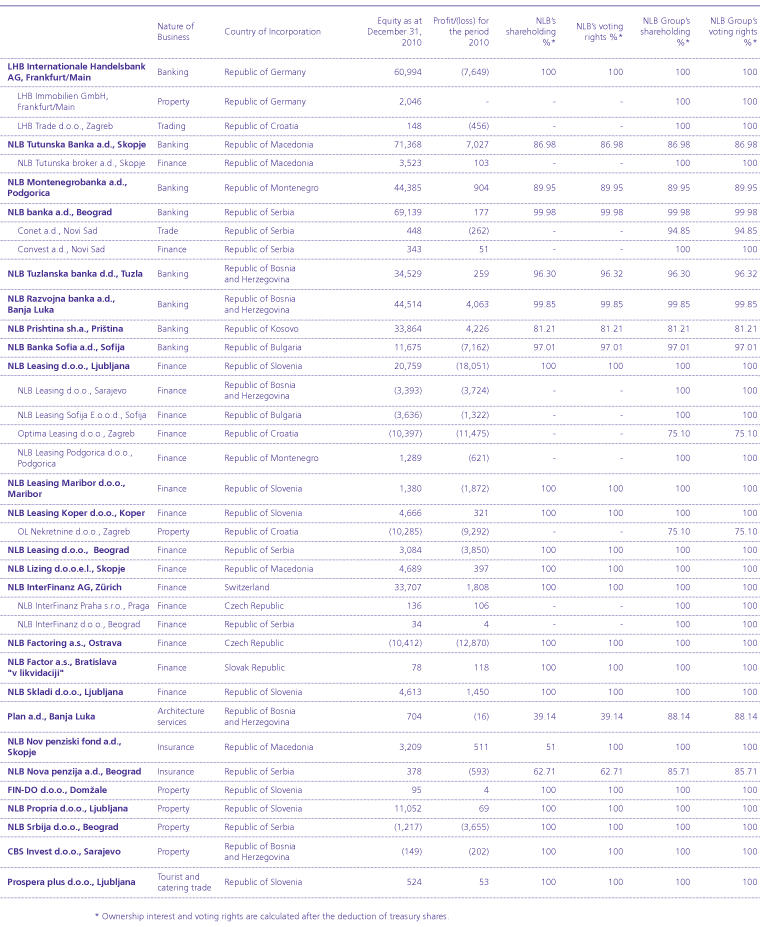

The NLB Group’s subsidiaries are presented in note 5.14.

2.5. Investments in subsidiaries, associates and joint ventures

In the separate financial statements, investments in subsidiaries, associates and joint ventures are accounted for at cost. Dividends from a subsidiaries, joint ventures or associates are recognized in income statement when NLB’s right to receive the dividend is established.

In the consolidated financial statements, investments in associates are accounted for using the equity method of accounting. These are undertakings in which the NLB Group generally holds between 20% and 50% of voting rights, and over which the NLB Group exercises significant influence, but does not have control.

The NLB Group’s share of its associates’ postacquisition profits or losses is recognized in the income statement, its share of other comprehensive income is recognized in other comprehensive income. The cumulative post-acquisition movements are adjusted against the carrying amount of the investment. When the NLB Group’s share of losses in an associate equals or exceeds its interest in the associate, including any other unsecured receivables, the NLB Group does not recognize further losses, unless it has incurred obligations or made payments on behalf of the associate.

Joint ventures are those entities over whose activities the NLB Group has joint control, as established by contractual agreement. In the consolidated financial statements investments in joint ventures are accounted for using the equity method of accounting.

The NLB Group’s principal associates and joint ventures are presented in note 5.14.

2.6. Goodwill and bargain purchases

Goodwill is measured by deducting the net assets of the acquiree from the aggregate of the consideration transferred for the acquiree, the amount of noncontrolling interest in the acquiree and fair value of an interest in the acquiree held immediately before the acquisition date. Any negative amount (“negative goodwill”) is recognized in profit or loss, after management reassesses whether it identified all the assets acquired and all liabilities and contingent liabilities assumed and reviews appropriateness of their measurement.

The consideration transferred for the acquiree is measured at the fair value of the assets given up, equity instruments issued and liabilities incurred or assumed, including fair value of assets or liabilities from contingent consideration arrangements but excludes acquisition related costs such as advisory, legal, valuation and similar professional services. Transaction costs incurred for issuing equity instruments are deducted from equity; transaction costs incurred for issuing debt are deducted from its carrying amount and all other transaction costs associated with the acquisition are expensed.

The goodwill of associates and joint ventures is included in the carrying value of investments.

2.7. Mergers of NLB Group entities

A merger of entities within the NLB Group is a business combination involving entities under common control. For such mergers the NLB Group applies merger accounting principles and uses the carrying amounts of merged entities, as reported in the consolidated financial statements. No goodwill arises on mergers of NLB Group entities and any difference between net assets merged and the cost of investment is recorded directly in equity.

Mergers of entities within the NLB Group do not affect the consolidated financial statements.

2.8. Foreign currency translation

Functional and presentation currency

Items included in the financial statements of each of the NLB Group's entities are measured using the currency of the primary economic environment in which the entity operates (i.e. the functional currency). The financial statements are presented in euros, which is the NLB Group’s presentation currency.

Transactions and balances

Foreign currency transactions are translated into the functional currency at the exchange rates prevailing at the dates of the transactions. Foreign exchange gains and losses resulting from the settlement of such transactions and from the translation of monetary assets and liabilities denominated in foreign currencies are recognized in the income statement, except when deferred in other comprehensive income as qualifying cash flow hedges.

Translation differences resulting from changes in the amortized cost of monetary items denominated in foreign currency and classified as available for sale financial assets, are recognized in the income statement.

Translation differences on non-monetary items, such as equities at fair value through profit or loss, are reported as part of the fair value gain or loss in the income statement. Translation differences on nonmonetary items, such as equities classified as available for sale, are included together with valuation reserves in the valuation (losses)/gains taken to other comprehensive income and accumulated in revaluation reserve in equity.

Gains and losses resulting from foreign currency purchases and sales for trading purposes are included in the income statement as gains less losses from financial assets and liabilities held for trading.

NLB Group entities

The financial statements of all the NLB Group entities that have a functional currency different from the presentation currency are translated into the presentation currency as follows:

- assets and liabilities for each statement of financial position presented are translated at the closing rate at the reporting date;

- income and expenses for each income statement are translated at average exchange rates;

- components of equity are translated at the historic rate; and

- all resulting exchange differences are recognized in other comprehensive income.

Goodwill and fair value adjustments arising from the acquisition of a foreign entity are treated as assets and liabilities of the foreign entity and translated at the closing rate.

During consolidation, exchange differences arising from the translation of the net investment in foreign operations are transferred to other comprehensive income. When control over a foreign operation is lost, the previously recognized exchange differences on translations to a different presentation currency are reclassified from other comprehensive income to profit and loss for the year as part of the gain or loss on disposal. On partial disposal of a subsidiary without loss of control, the related portion of accumulated currency translation differences is reclassified to noncontrolling interest within equity.

2.9. Interest income and expenses

Interest income and expenses are recognized in the income statement for all interest-bearing instruments on an accrual basis using the effective interest rate method. The effective interest rate method is a method used to calculate the amortized cost of a financial asset or financial liability and to allocate the interest income or interest expense over the relevant period. The effective interest rate is the rate that precisely discounts estimated future cash payments or receipts over the expected life of the financial instrument or a shorter period when appropriate, to the net carrying amount of the financial asset or financial liability. Interest income includes coupons earned on fixed-yield investments and trading securities and accrued discounts and premiums on securities. The calculation of the effective interest rate includes all fees and points paid or received between parties to the contract and all transaction costs, but excludes future credit risk losses. Once a financial asset or a group of similar financial assets has been impaired, interest income is recognized using the rate of interest used to discount the future cash flows for the purpose of measuring the impairment loss.

2.10. Fee and commission income

Fees and commissions are generally recognized when the service has been provided. Fees and commissions consist mainly of fees received from payment services and from the managing of funds on behalf of legal entities and individuals, together with commissions from guarantees. Fees and commissions that are integral to the effective interest rate of financial assets and liabilities are presented within interest income or expenses.

2.11. Dividend income

Dividends are recognized in the income statement when the NLB Group’s right to receive payment is established and inflow of economic benefits is probable. In consolidated financial statement dividends received from associates and joint ventures reduce the carrying value of the investment.

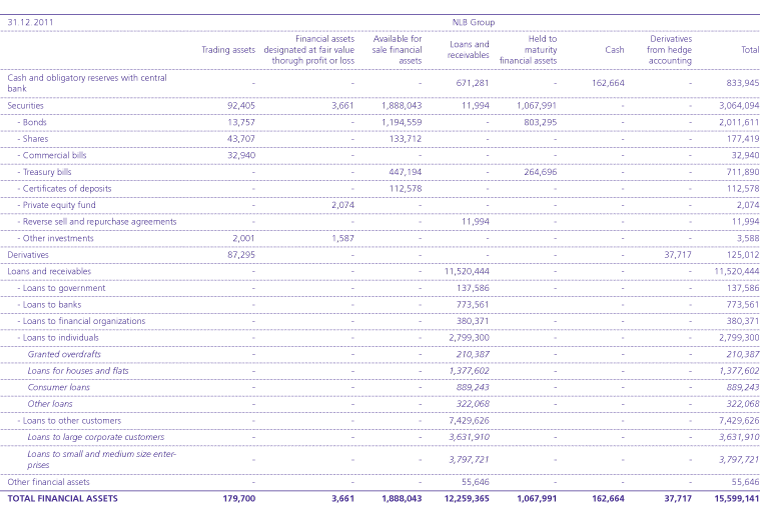

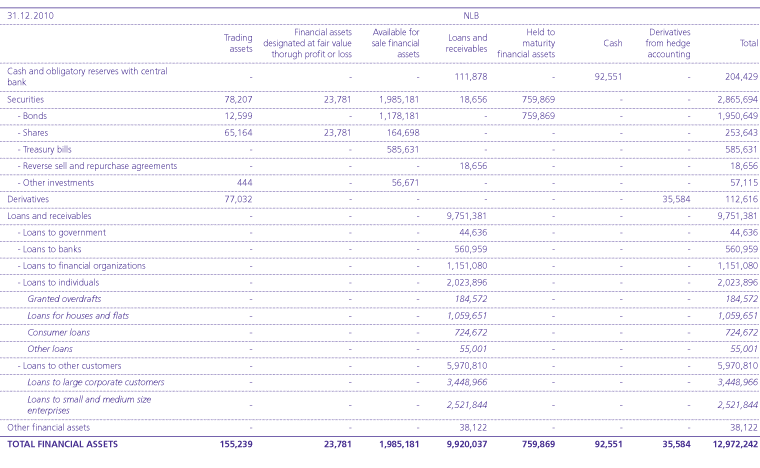

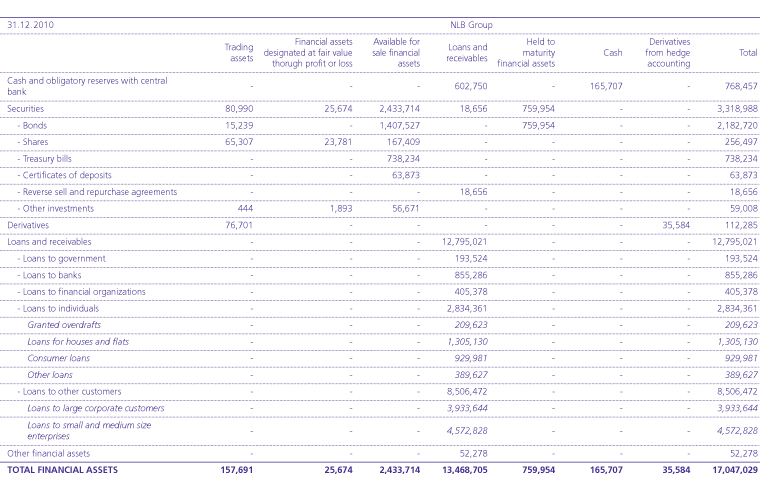

2.12. Financial instruments

a) Classification

The classification of financial instruments on initial recognition depends on the instruments’ characteristics and management’s intention. In general, the following criteria are taken into account:

Financial instruments at fair value through profit or loss

This category has two sub-categories: financial instruments held for trading and financial instruments designated at fair value through profit or loss at inception. A financial instrument is classified in this group if acquired principally for the purpose of selling in the short term or if so designated by management.

The NLB Group designates financial instruments at fair value through profit or loss if:

- it eliminates or significantly reduces a measurement or recognition inconsistency that would otherwise arise from measuring assets or liabilities on a different basis;

- a group of financial assets, financial liabilities or both is managed and its performance is evaluated on a fair value basis, in accordance with a documented risk management or investment strategy, and information about the group is provided internally on that basis to the NLB Group’s key management; or

- a financial instrument contains one or more embedded derivatives that could significantly modify the cash flows otherwise required by the contract.

Derivatives are also categorized as held for trading unless they are designated as hedging instruments.

Loans and advances

Loans and advances are non-derivative financial instruments with fixed or determinable payments that are not quoted on an active market, other than: (a) those that the NLB Group intends to sell immediately or in the short term, which are classified as held for trading, and those that the NLB Group, upon initial recognition, classifies at fair value through profit or loss; (b) those that the NLB Group, upon initial recognition, classifies as available for sale; or (c) those for which the NLB Group may not recover substantially all of its initial investment, for reasons other than deterioration in creditworthiness.

Held to maturity investments

Held to maturity investments are non-derivative financial instruments that are traded in an active market with fixed or determinable payments and a fixed maturity that the NLB Group has both the intention and ability to hold to maturity. An investment is not classified as held to maturity investment if the NLB Group has the right to require that the issuer repays or redeems the investment before its maturity, because paying for such a feature is inconsistent with expressing an intention to hold the assets until the maturity.

Available for sale financial assets

Available for sale financial assets are those intended to be held for an indefinite period of time, which may be sold in response to needs for liquidity or changes in interest rates, exchange rates or equity prices.

b) Measurement and recognition

Financial assets are initially recognized at fair value plus transaction costs for all financial assets not carried at fair value through profit or loss.

Financial assets carried at fair value through profit or loss are initially recognized at fair value and transaction costs are expensed in the income statement.

Regular way purchases and sales of financial assets at fair value through profit or loss, and assets held to maturity and available for sale, are recognized on the trade date. Loans and advances are recognized when cash is advanced to the borrowers.

Financial assets at fair value through profit or loss and available for sale financial assets are subsequently measured at fair value. Gains and losses from changes in the fair value of financial assets at fair value through profit or loss are included in the income statement in the period in which they arise. Gains and losses from changes in the fair value of available for sale financial assets are recognized in other comprehensive income until the financial asset is derecognized or impaired, at which time the cumulative amount previously included in other comprehensive income is recycled in the income statement. However, interest calculated using the effective interest rate method and foreign currency gains and losses on monetary assets classified as available for sale are recognized in the income statement. Dividends on available for sale equity instruments are recognized in the income statement when the NLB Group’s right to receive payment is established.

Loans and held to maturity investments are carried at amortized cost.

c) Day one gains or losses

The best evidence of fair value at initial recognition is the transaction price (i.e. the fair value of the consideration given or received), unless the fair value of that instrument is evidenced by comparison with other observable current market transactions in the same instrument (i.e. without modification or repackaging) or based on a valuation technique whose variables include only data from observable markets.

If the transaction price on a non-active market is different than the fair value from other observable current market transactions in the same instrument or is based on a valuation technique whose variables include only data from observable markets, the difference between the transaction price and fair value is recognized immediately in the income statement (“day one gains or losses”).

In cases where the data used for valuation is not fully observable in financial markets, day one gains or losses are not recognized immediately in the income statement. The timing of recognition of deferred day one gains or losses is determined individually. It is either amortized over the life of the transaction, deferred until the instrument’s fair value can be determined using market observable inputs or realized through settlement.

d) Reclassification

Financial assets that are eligible for classification as loans and advances can be reclassified out of the held for trading category if they are no longer held for the purpose of selling or repurchasing them in the near term. Financial assets that are not eligible for classification as loans and receivables may be transferred from the held for trading category only in rare circumstances. Additionally, instruments designated at fair value through profit and loss cannot be reclassified.

e) Derecognition

A financial asset is derecognized when the contractual rights to the cash flows from the financial asset expire or the financial asset is transferred and the transfer qualifies for derecognition. A financial liability is derecognized only when it is extinguished, i.e. when the obligation specified in the contract is discharged, cancelled or expires.

f) Fair value measurement principles

The fair value of financial instruments traded on active markets is based on the current bid price at the reporting date, excluding transaction costs. If there is no active market, the fair value of the instruments is estimated using discounted cash flow techniques or pricing models.

If discounted cash flow techniques are used, estimated future cash flows are based on management’s best estimates and the discount rate is a market based rate at the reporting date for an instrument with similar terms and conditions. If pricing models are used, inputs are based on market based measurements at the reporting date.

g) Derivative financial instruments and hedge accounting

Derivative financial instruments, including forward and futures contracts, swaps and options, are initially recognized in the statement of financial position at fair value. Derivative financial instruments are subsequently re-measured at their fair value. Fair values are obtained from quoted market prices, discounted cash flow models or pricing models, as appropriate. All derivatives are carried at their fair value within assets when the derivative position is favourable to the NLB Group and within liabilities when the derivative position is unfavourable to the NLB Group.

The method of recognizing the resulting fair value gain or loss depends on whether the derivative is designated as a hedging instrument, and if so, the nature of the item being hedged. The NLB Group designates certain derivatives as either:

- hedges of the fair value of recognized assets or liabilities or firm commitments (fair value hedge),

- hedges of highly probable future cash flows attributable to a recognized asset or liability, or a highly probable forecasted transaction (cash flow hedge) or

- hedges of a net investment in a foreign operation (net investment hedge).

Hedge accounting is used for derivatives designated in this way provided certain criteria are met.

The NLB Group documents, at the inception of the transaction, the relationship between hedged items and hedging instruments, as well as its risk management objective and strategy for undertaking various hedge transactions. The NLB Group also documents its assessment, both at hedge inception and on an ongoing basis, whether the derivatives that are used in hedging transactions are highly effective in offsetting changes in fair values or cash flows of hedged items. The actual results of a hedge must always fall within a range of 80% to 125%.

Fair value hedge

Changes in the fair value of derivatives that are designated and qualify as fair value hedges are recognized in the income statement, together with any changes in the fair value of the hedged asset or liability that are attributable to the hedged risk. Effective changes in the fair value of hedging instruments and related hedged items are reflected in “fair value adjustments in hedge accounting” in the income statement. Any ineffectiveness is recorded in “Gains less losses on financial assets and liabilities held for trading”.

If a hedge no longer meets the hedge accounting criteria, the adjustment to the carrying amount of the hedged item for which the effective interest rate method is used is amortized to profit or loss over the remaining period to maturity. The adjustment to the carrying amount of a hedged equity security is included in the income statement upon disposal of the equity security.

Cash flow hedge

The effective portion of changes in the fair value of derivatives that are designated and qualify as cash flow hedges is recognized in other comprehensive income. The gain or loss relating to the ineffective portion is recognized immediately in the income statement in “Gains less losses on financial assets and liabilities held for trading”.

Amounts accumulated in equity are recycled as a reclassification from other comprehensive income to the income statement in the periods when the hedged item affects profit or loss.

When a hedging instrument expires or is sold, or when a hedge no longer meets hedge accounting criteria, any cumulative gain or loss existing in other comprehensive income and previously accumulated in equity at that time remains in other comprehensive income and in equity and is recognized in profit or loss only when the forecasted transaction is ultimately recognized in the income statement. When a forecasted transaction is no longer expected to occur, the cumulative gain or loss that was reported in other comprehensive income is immediately transferred to the income statement.

Hedge of a net investment in a foreign operation

Hedges of net investments in foreign operations are accounted for similarly to cash flow hedges. Any gain or loss on the hedging instrument relating to the effective portion of the hedge is recognized directly in equity. The gain or loss relating to the ineffective portion is recognized immediately in the consolidated income statement in “Gains less losses on financial assets and liabilities held for trading”. Gains and losses accumulated in other comprehensive income are included in the consolidated income statement when the foreign operation is disposed of as part of the gain or loss on the disposal.

In the separate financial statements the hedge of the net investment in foreign operation is accounted for as fair value hedge.

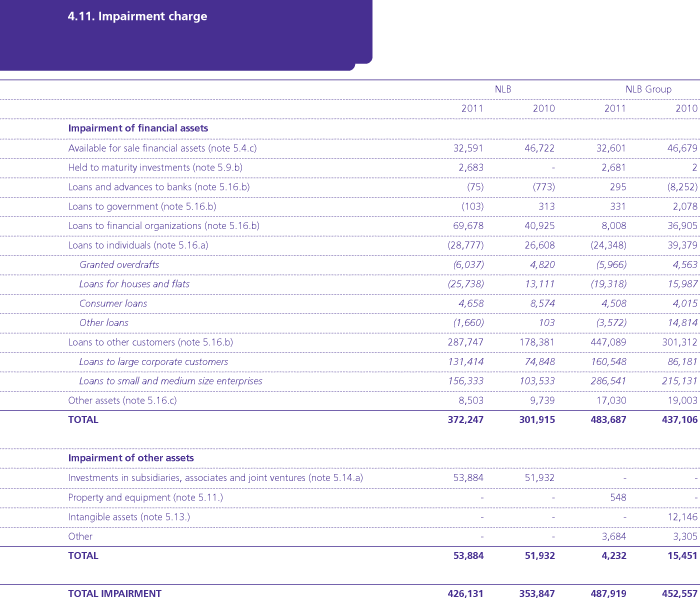

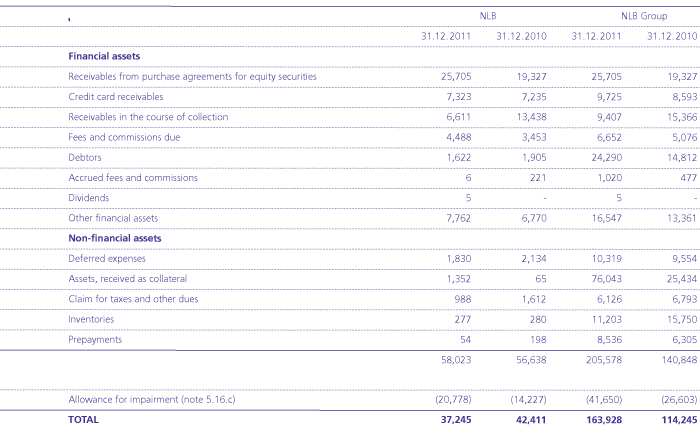

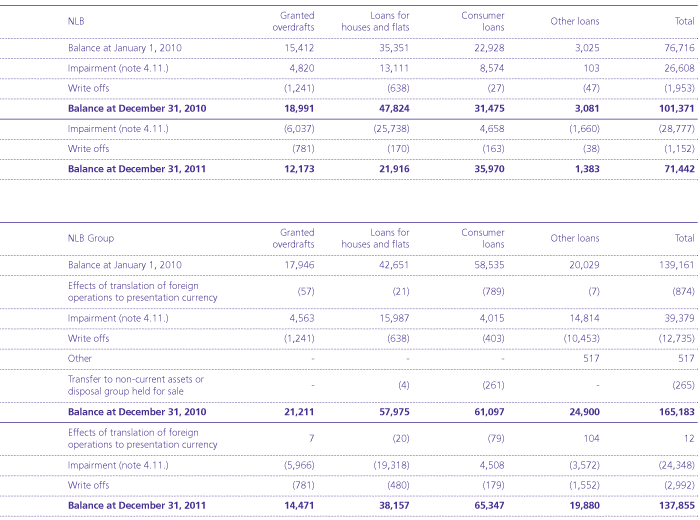

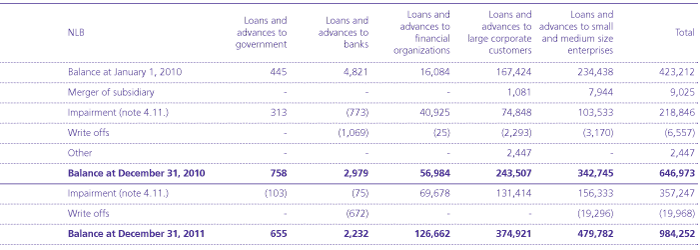

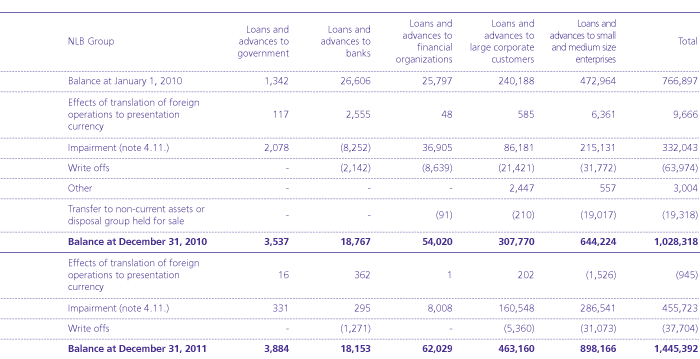

2.13. Impairment of financial assets

a) Assets carried at amortized cost

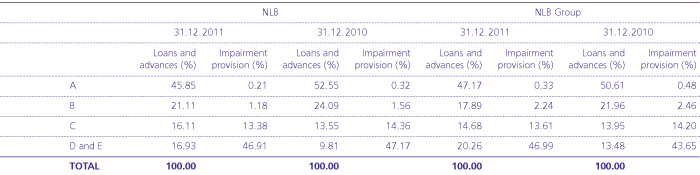

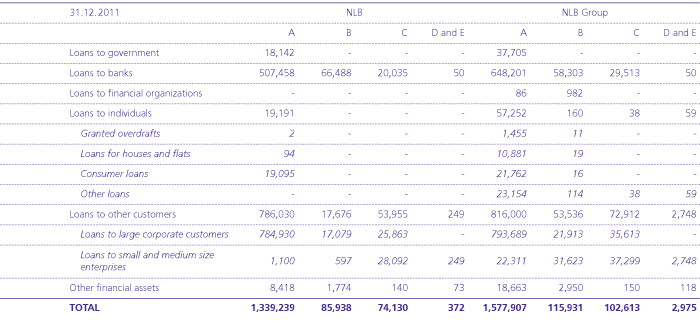

The NLB Group assesses impairments of financial assets individually for all individually significant assets where there is objective evidence of impairment; all other financial assets are impaired collectively. According to the Regulation on credit risk loss assessment of the Bank of Slovenia financial asset or off-balance sheet liability is individually significant if total exposure to the client exceeds 0.5% of bank’s equity. In years 2011 and 2010 all exposures to banks, all exposures to other legal entities with A and B rating whose exposure exceeds EUR 6,500 thousand, all legal entities rated C, whose exposure exceeds EUR 500 thousand and all exposures to D and E legal entities, whose exposure exceeds EUR 10 thousand are considered individually significant assets by NLB. If the NLB Group determines that no objective evidence of impairment exists for an individually assessed financial asset, it includes the asset in a group of financial assets with similar credit risk characteristic and collectively assesses them for impairment.

The NLB Group assesses at each reporting date whether there is objective evidence that a financial asset or group of financial assets is impaired. A financial asset or group of financial assets is impaired and impairment losses are incurred if, and only if, there is objective evidence of impairment as a result of one or more events that occurred after the initial recognition of the asset and that event has an impact on the future cash flows of the financial asset or group of financial assets that can be reliably estimated.

The criteria that the NLB Group uses to determine that there is objective evidence of an impairment loss include:

- delinquency in contractual payments of principal or interest;

- cash flow difficulties experienced by the borrower;

- breach of loan covenants or conditions;

- initiation of bankruptcy proceedings;

- deterioration of the borrower’s competitive position;

- deterioration in the value of collateral; and

- downgrading below investment grade level.

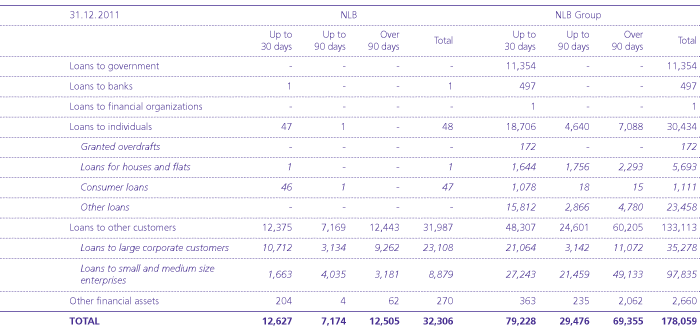

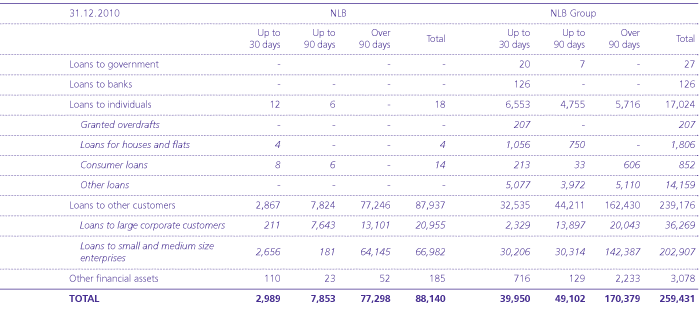

The estimated period between the occurrence of problems, which prevent the client from paying his obligations to the NLB Group, and identification of these problems by the NLB Group varies from between three and six months.

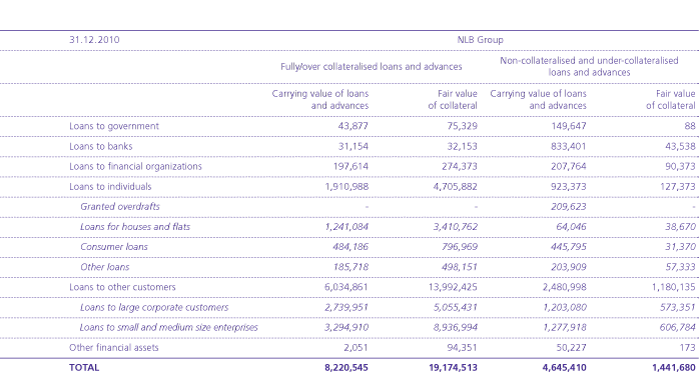

If there is objective evidence that an impairment loss on loans and advances or held to maturity investment has been incurred, the amount of the loss is measured as the difference between the asset’s carrying amount and the present value of estimated future cash flows. The carrying amount of the asset is reduced through an allowance account and the amount of the loss is recognized in the income statement. The calculation of the present value of the estimated future cash flows of collateralized financial assets reflects the cash flows that may result from foreclosure, less cost of obtaining and selling the collateral. Off-balance sheet liabilities are also assessed individually and where necessary related provision are recognized as liabilities.

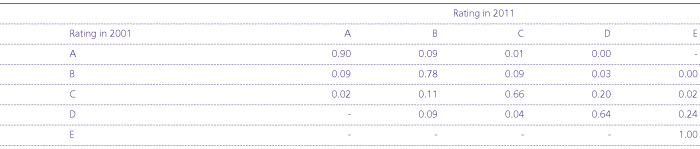

For the purpose of collective evaluation of impairment, the NLB Group uses migration matrices, which illustrate the expected migration of customers between internal rating classes. The probability of migration is assessed on the basis of past years’ experience, i.e. annual migration matrices for different types of customers. These data may be adopted for the predicted future trends since historic experience does not necessarily reflect the actual economic movements. Exposures to individuals are additionally analyzed with regard to type of products. Based on the expected migration of clients to D and E rating class and assessment of average repayment rate for D and E rated customers, the NLB Group recognizes collective impairments.

If the amount of impairment subsequently decreases due to an event occurring after the write down, the reversal of the loss is recognized as a reduction in the allowance for loan impairment.

When a loan is uncollectible, it is written off against the related allowance for loan impairment. Such loans are written off after all the necessary procedures have been completed and the amount of the loss has been determined. Subsequent recoveries of amounts previously written off decrease the amount of the provision for loan impairment in the income statement.

The objective criteria that the NLB Group uses to determine that a loan should be written off include:

- the debtor no longer performs his regular activities (termination of the legal entity);

- the NLB Group holds no adequate collateral to be used for repayment; and

- judicial recovery proceedings have been concluded.

b) Assets classified as available for sale

The NLB Group assesses at each reporting date whether there is objective evidence that available for sale financial assets are impaired. In the case of equity investments classified as available for sale, a significant or prolonged decline in the fair value of a security below its cost is considered in determining whether the assets are impaired. If any such evidence exists for available for sale financial assets, the cumulative loss is reclassified from other comprehensive income and recognized in the income statement as an impairment loss. Impairment losses recognized in the income statement on equity instruments are not reversed through the income statement; subsequent increases in their fair value after impairment are recognized in other comprehensive income.

If, in a subsequent period, the fair value of a debt instrument classified as available for sale increases and the increase can be objectively related to an event occurring after the impairment loss was recognized, the impairment loss is reversed through the income statement.

The following factors are considered in determining impairment losses on debt instruments:

- default or delinquency in interest or principal payments,

- liquidity difficulties of the issuer,

- breach of contract covenants or conditions,

- bankruptcy of the issuer,

- deterioration of economic and market conditions and

- deterioration in the credit rating of the issuer below the acceptable level.

Impairment losses recognized in the income statement are measured as the difference between the carrying amount of the financial asset and its current fair value. The current fair value of the instrument is its market price or discounted future cash flows, when the market price is not obtainable.

c) Renegotiated loans

Loans that are subject to either collective or individual impairment assessment and whose terms have been renegotiated due to deterioration of the borrower’s financial position are no longer considered to be past due but are treated as new loans. Such loans continue to be discounted using the original effective interest rate.

d) Repossessed assets

In certain circumstances, assets are repossessed following the foreclosure on loans that are in default. Repossessed assets are initially recognized in the financial statements at their fair values and are sold as soon as practical in order to reduce exposure (note 7.1.j). After initial recognition, repossessed assets are measured and accounted for in accordance with the policies applicable for the relevant assets categories.

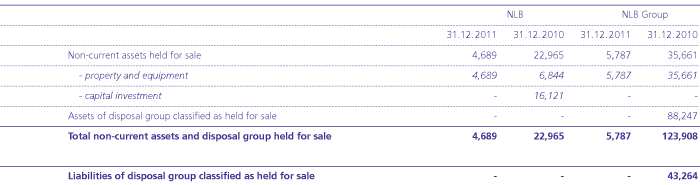

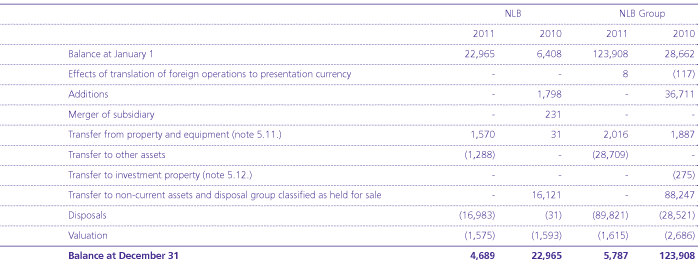

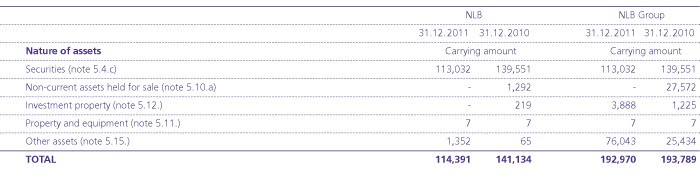

In 2011 the NLB Group changed the accounting policy regarding the initial recognition for repossessed assets. Due to that repossessed assets in amount of EUR 1,288 thousand in NLB (December 31, 2010: EUR 1,292 thousand) and in the NLB Group in amount of EUR 28,709 thousand (December 31, 2010: EUR 27,572 thousand) were reclassified from non-current assets and disposal group held for sale to other assets (note 5.10.d).

2.14. Offsetting

Financial assets and liabilities are offset and the net amount reported in the statement of financial position when there is a legally enforceable right to offset the recognized amounts and there is an intention to settle on a net basis, or to realize the asset and settle the liability simultaneously.

2.15. Sale and repurchase agreements

Securities sold under sale and repurchase agreements (repos) are retained in the financial statements and the counterparty liability is included in financial liabilities associated with the transferred assets. Securities sold subject to sale and repurchase agreements are reclassified in the financial statements as pledged assets when the transferee has the right by contract or custom to sell or re-pledge the collateral. Securities purchased under agreements to resell (reverse repos) are recorded as loans and advances to other banks or customers, as appropriate.

The difference between the sale and repurchase price is treated as interest and accrued over the life of the repo agreements using the effective interest rate method.

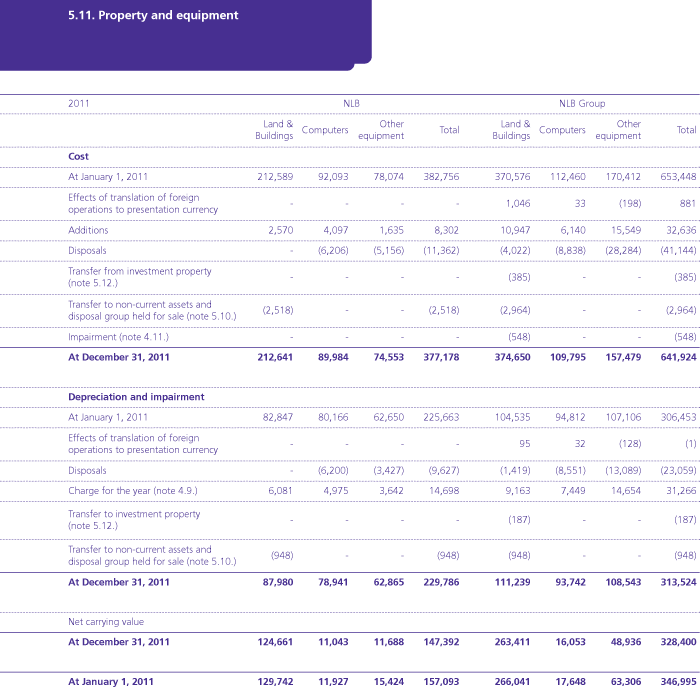

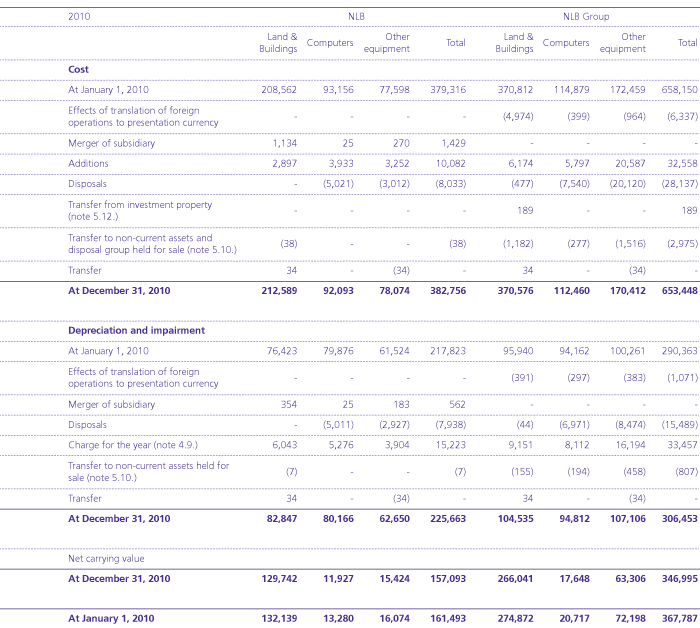

2.16. Property and equipment

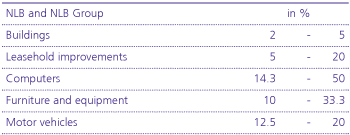

All items of property and equipment are initially recognized at cost. They are subsequently measured at cost less accumulated depreciation and any accumulated impairment loss.

Each year, the NLB Group assesses whether there are indications that assets may be impaired. If any such indication exists, the recoverable amounts are estimated. The recoverable amount is the higher of the fair value less costs to sell and value in use. If the recoverable amount exceeds the carrying value, the assets are not impaired. If the carrying amount exceeds the recoverable amount, the difference is recognized as a loss in the income statement.

Items of property and equipment, which do not generate cash flows that are largely independent, are included in cash generating unit and later tested for possible impairment.

Depreciation is calculated on a straight-line basis over the assets’ estimated useful lives. The following annual depreciation rates were applied:

Depreciation does not begin until the assets are available for use.

The assets' residual values and useful lives are reviewed, and adjusted if appropriate, on each reporting date.

Gains and losses on the disposal of items of property and equipment are determined as a difference between the sale proceeds and their carrying amount, and are recognized in the income statement.

Maintenance and repairs are charged to the income statement during the financial period in which they are incurred. Subsequent costs that increase future economic benefits are recognized in the carrying amount of an asset and the replaced part, if any, is derecognized.

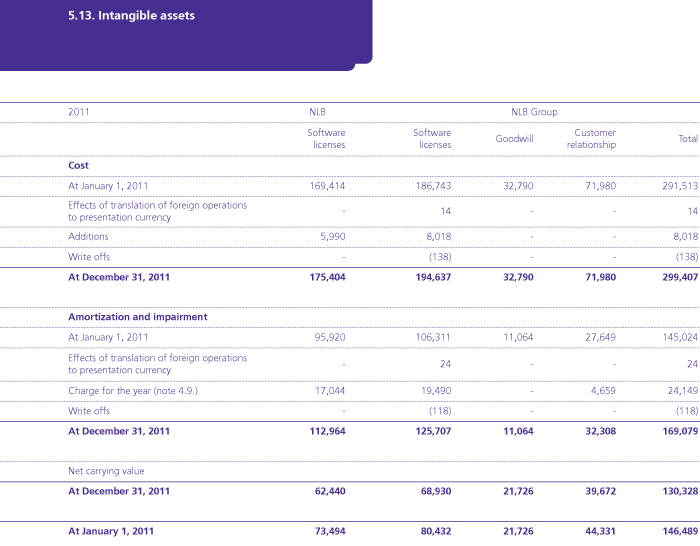

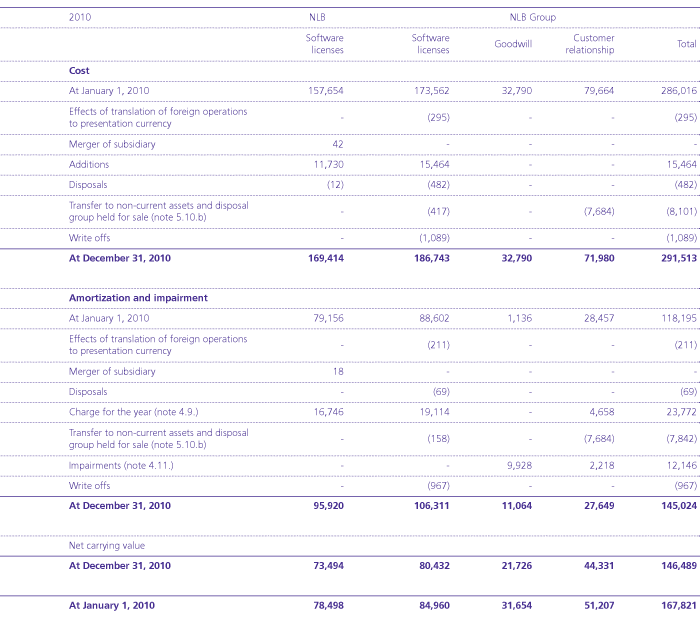

2.17. Intangible assets

Intangible assets include software licenses, goodwill (note 2.6.) and customer relationships. Intangible assets are stated at cost, less accumulated amortization and impairment losses.

Amortization is calculated on a straight-line basis at rates designed to write down the cost of intangible asset over its estimated useful life. The core banking system is amortized over a period of ten years, other software over a period of three to five years and customer relationships over a period of twelve to fifteen years.

Amortization does not begin until the assets are available for use.

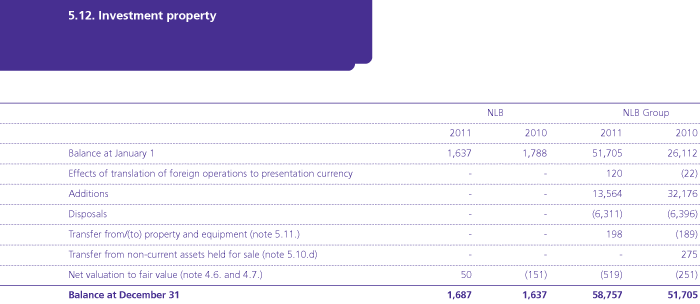

2.18. Investment property

Investment property includes buildings held for leasing and not occupied by the NLB Group. Investment property is stated at fair value determined by a certified appraiser. Fair value is based on current market prices. Any gain or loss arising from a change in fair value is recognized in the income statement. If there is a change in use due to the commencement of owner occupation, investment property is transferred to owner occupied property.

2.19. Non-current assets and disposal group classified as held for sale

Non-current assets and disposal group are classified as held for sale if their carrying amount will be recovered through a sale transaction rather than through continuing use. This condition is deemed to be met only when the sale is highly probable and the asset is available for immediate sale in its present condition. Management must be committed to the sale, which should be expected to qualify for recognition as a completed sale within one year from the date of classification. Non-current assets and disposal group classified as held for sale are measured at the lower of the assets’ previous carrying amount and fair value less costs to sell.

During subsequent measurement, certain assets and liabilities of disposal group that are outside the scope of IFRS 5 measurement requirements are measured in accordance with the applicable standards (e.g. deferred tax assets, assets arising from employee benefits, financial instruments, investment property measured at fair value and contractual rights under insurance contracts). Tangible and intangible assets are not depreciated. The effects of sale and valuation are included in the income statement as a gain or loss from non-current assets held for sale.

Liabilities directly associated with disposal groups are reclassified and presented separately in the statement of financial position.

2.20. Accounting for leases

A lease is an agreement whereby the lessor conveys to the lessee, in return for a payment or series of payments, the right to use an asset for an agreed period of time. Lease agreements are accounted for in accordance with their classification as finance leases or operating leases at the inception of the lease. The key classification factor is the extent to which the risks and rewards incidental to ownership of a leased asset lie with the lessor or lessee.

The NLB Group as lessee

Leases in which a significant portion of the risk and rewards of ownership are retained by the lessor are classified as operating leases. Payments made under operating leases are charged to the income statement on a straight-line basis over the period of the lease. When an operating lease is terminated before the lease period has expired, any payment required to be made to the lessor by way of penalty is recognized as an expense in the period in which termination takes place.

Finance leases are recognized as an asset and liability at amounts equal to the fair value of the leased asset or, if lower, the present value of the minimum lease payments. Leased assets are depreciated in accordance with the NLB Group’s policy over the shorter of the estimated useful life of the asset and the lease term, if there is no reasonable certainty that the NLB Group will obtain ownership by the end of the lease term. Lease payments are apportioned between interest expenses and the reduction of the outstanding liability so as to produce constant periodic rate of interest on the remaining balance of the liability.

The NLB Group as lessor

Payments under operating leases are recognized as income on a straight-line basis over the period of the lease. Assets leased under operating leases are presented in the statement of financial position as investment property or as property and equipment.

The NLB Group classifies a lease as a finance lease when the risks and rewards incidental to ownership of a leased asset lie with the lessee. When assets are leased under a finance lease, the present value of the lease payments is recognized as a receivable. Income from finance lease transactions is amortized over the lifetime of the lease using the effective interest rate method. Finance lease receivables are recognized at an amount equal to the net investment in the lease, including the unguaranteed residual value.

Sale-and-leaseback transactions

The NLB Group also enters into sale-and-leaseback transactions (in which the NLB Group is primarily a lessor), under which the leased assets are purchased from and then leased back to the lessee. These contracts are classified as finance leases or operating leases, depending on the contractual terms of the leaseback agreement.

2.21. Cash and cash equivalents

For the purpose of the statement of cash flows, cash and cash equivalents comprise cash and balances with central banks, debt securities held for trading, loans to banks and debt securities not held for trading with an original maturity of up to 90 days. Cash and cash equivalents are disclosed under the cash flow statement.

2.22. Borrowings

Borrowings are initially recognized at fair value net of transaction costs. Borrowings are subsequently stated at amortized cost and any difference between the amount initially recognized and the redemption value is recognized in the income statement over the period of the borrowings using the effective interest rate method.

If the NLB Group purchases its own debt, it is derecognized from the statement of financial position. Any difference between the carrying amount of the purchased debt and the amount paid is recognized immediately in the income statement.

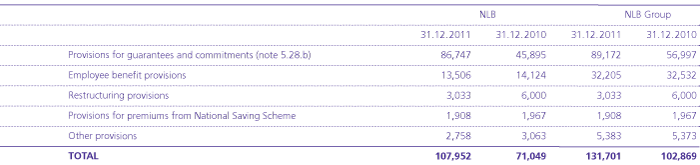

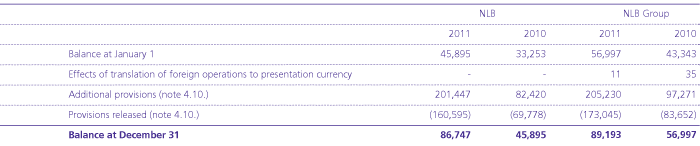

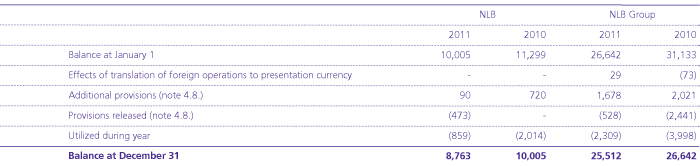

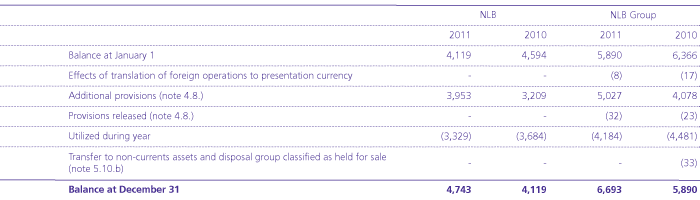

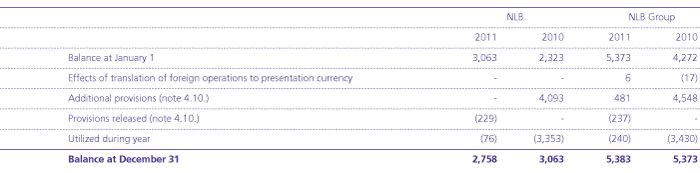

2.23. Provisions

Provisions are recognized when the NLB Group has a present legal or constructive obligation as a result of past events and it is probable that an outflow of resources embodying economic benefits will be required to settle the obligation and a reliable estimate of the amount of the obligation can be made.

2.24. Financial guarantees

Financial guarantees are contracts that require the issuer to make specific payments to reimburse the holder for a loss it incurs because a specific debtor fails to make payments when due, in accordance with the terms of debt instruments. Such financial guarantees are given to banks, financial institutions and other bodies on behalf of the customer to secure loans, overdrafts and other banking facilities.

Financial guarantees are initially recognized at fair value, which is normally evidenced by the fees received. The fees are amortized to the income statement over the contract term using the straightline method. The NLB Group’s liabilities under guarantees are subsequently measured at the greater of:

- the initial measurement, less amortization calculated to recognize fee income over the period of guarantee or

- the best estimate of the expenditure required to settle the obligation.

2.25. Inventories

Inventories are measured at the lower of cost and net realizable value. Cost is determined using the weighted average cost method.

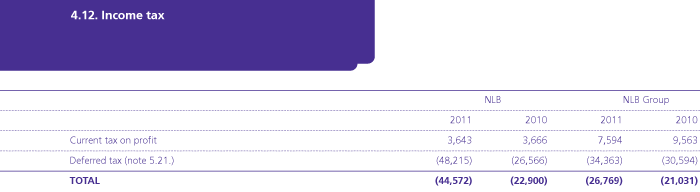

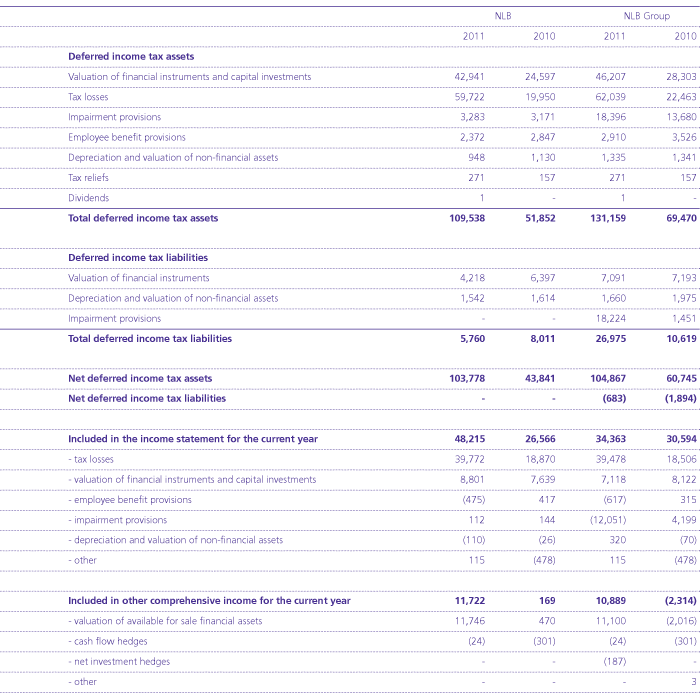

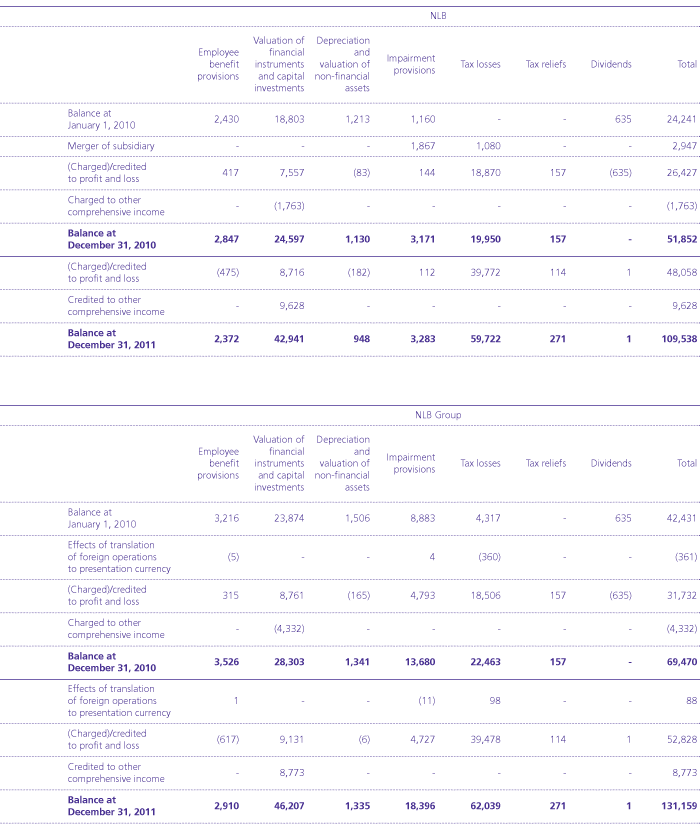

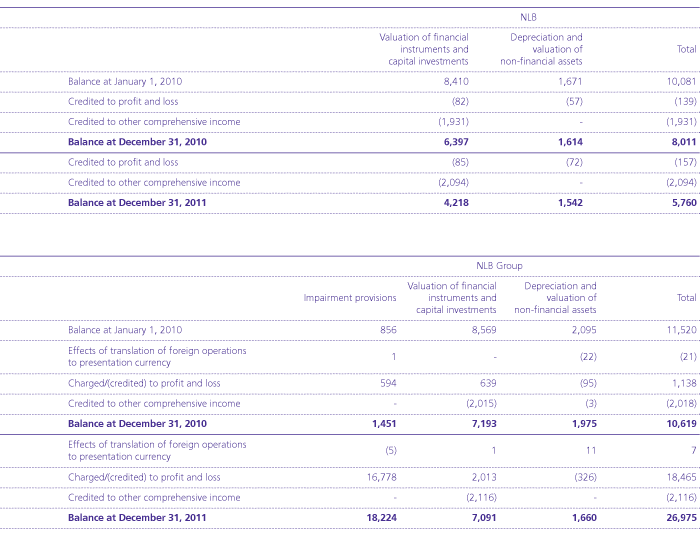

2.26. Taxes

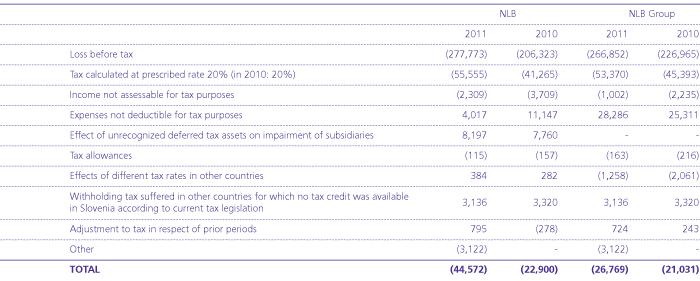

Income tax in the NLB Group is calculated on taxable profits at the applicable tax rate in the respective jurisdiction. The tax rate for 2011 in Slovenia is 20% (2010: 20%).

Deferred income tax is calculated, using the balance sheet liability method, for all temporary differences arising between the tax bases of assets and liabilities and their carrying amounts for financial reporting purposes.

Deferred tax assets are recognized if it is probable that future taxable profit will be available against which the temporary differences can be utilized.

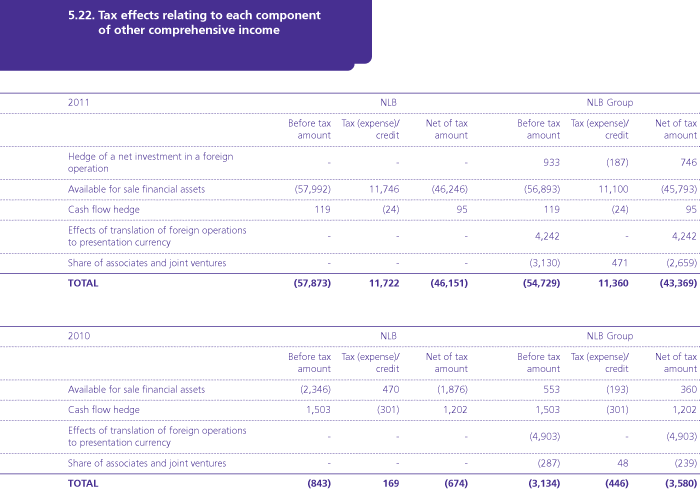

Deferred tax related to the fair value re-measurement of available for sale investments and cash flow hedges is charged or credited directly to other comprehensive income.

Deferred tax assets and liabilities are measured at tax rates enacted or substantively enacted at the end of the reporting period that are expected to apply to the period when the asset is realized or the liability is settled. At each reporting date, the NLB Group reviews the carrying amount of deferred tax assets and assesses future taxable profits against which temporary taxable differences can be utilized.

Deferred tax assets for temporary differences arising from investments in subsidiaries, associates and joint ventures are recognized only to the extent that it is probable that:

- the temporary differences will be reversed in the foreseeable future; and

- taxable profit will be available.

In 2011, the NLB Group recorded a net loss. The deferred tax assets recognized at December 31, 2011 are based on future profitability assumptions and business plans for future years. Tax assets may be adjusted in the event of changes to these assumptions.

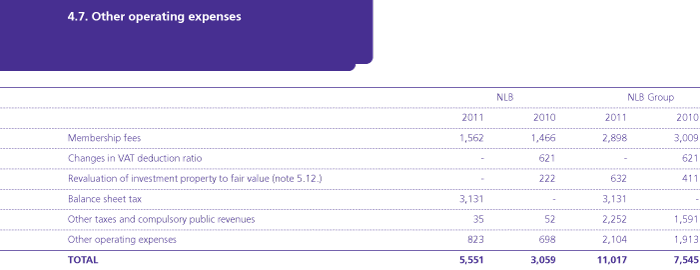

In 2011 a new tax on balance sheet was enforced, which is in NLB recognized in other operating expenses (note 4.7.).

Tax base for balance sheet tax is balance sheet volume, which represents value of assets in Statement of financial position. It is calculated as the average value of monthly values on the last day of each month in the calendar year. Tax rate for balance sheet is 0,1%.

Calculated tax may be reduced by 0,167% of loans granted to nonfinancial firms and independent entrepreneurs. Loans are calculated as the average value of monthly net balances without allowances for impairments or change in fair value on the last day of each month in the calendar year. For the year 2011 due to the provision of Tax on Balance Sheet Act, average balances on balance sheet volume and loans are calculated using monthly balances from August onwards.

2.27. Fiduciary activities

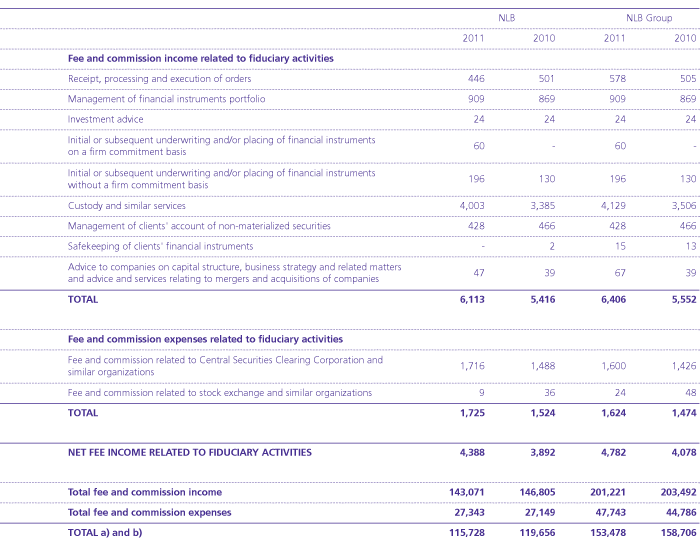

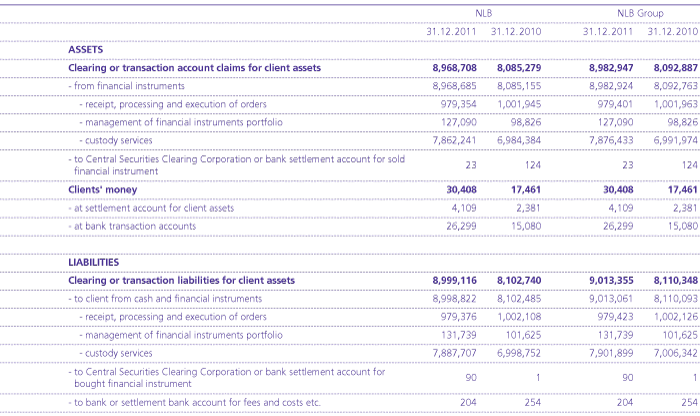

The NLB Group provides asset management services to its clients. Assets held in a fiduciary capacity are not reported in the NLB Group’s financial statements, as they do not represent assets of the NLB Group. Fee and commission income charged for this type of service is broken down by items in note 4.3.b). Further details on transactions managed on behalf of third parties are disclosed in note 5.29.

Based on the requirements of Slovenian legislation, the NLB Group has additionally disclosed in note 5.29. assets and liabilities on accounts used to manage financial assets from fiduciary activities, i.e. information related to the receipt, processing and execution of orders and related custody activities.

2.28. Employee benefits

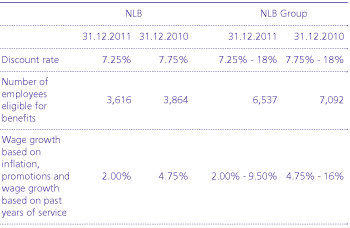

Employee benefits include jubilee long service benefits, retirement indemnity bonuses and termination benefits. Provisions for employee benefits are calculated by an independent actuary. The main assumptions included in the actuarial calculation are as follows:

According to legislation, employees retire after 35-40 years of service, when, if they fulfil certain conditions, they are entitled to a lump-sum severance payment. Employees are also entitled to a long service bonus for every ten years of service.

These obligations are measured at the present value of future cash outflows considering future salary increases and then apportioned to past and future employee service based on benefit plan terms and conditions. All gains and losses arising from changes in assumptions and experience adjustments are recognized immediately in the income statement.

The NLB Group pays contributions to the state pension schemes according to the local legislation.

NLB contributes 8.85% of gross salaries. Once contributions have been paid, the NLB Group has no further obligation. Contributions constitute costs in the period to which they relate and are disclosed in employee costs in the income statement.

2.29. Share capital

Dividends on ordinary shares

Dividends on ordinary shares are recognized in equity in the period in which they are approved by NLB’s shareholders.

Treasury shares

If NLB or other member of the NLB Group purchases NLB’s shares, the consideration paid is deducted from total shareholders’ equity as treasury shares. If such shares are subsequently sold, any consideration received is included in equity. If NLB's shares are purchased by NLB itself or other NLB Group entities, NLB creates reserves for treasury shares in equity.

Share issue costs

Costs directly attributable to the issue of new shares are recognized in equity as a reduction in the share premium account.

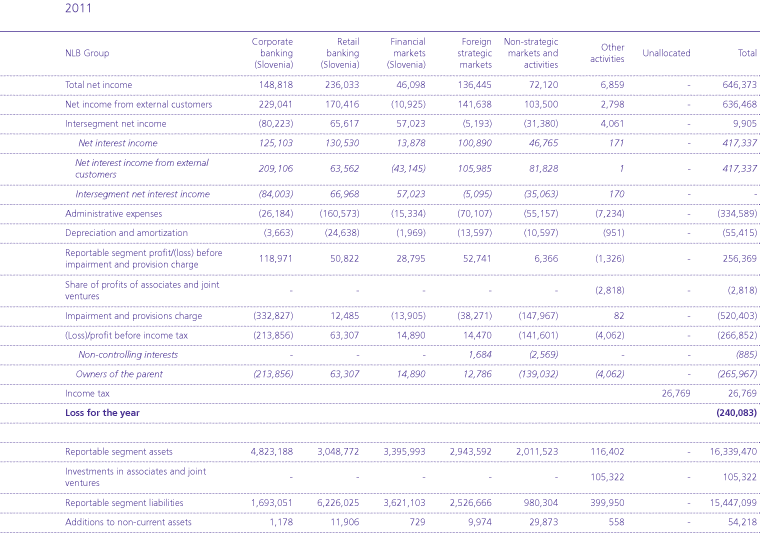

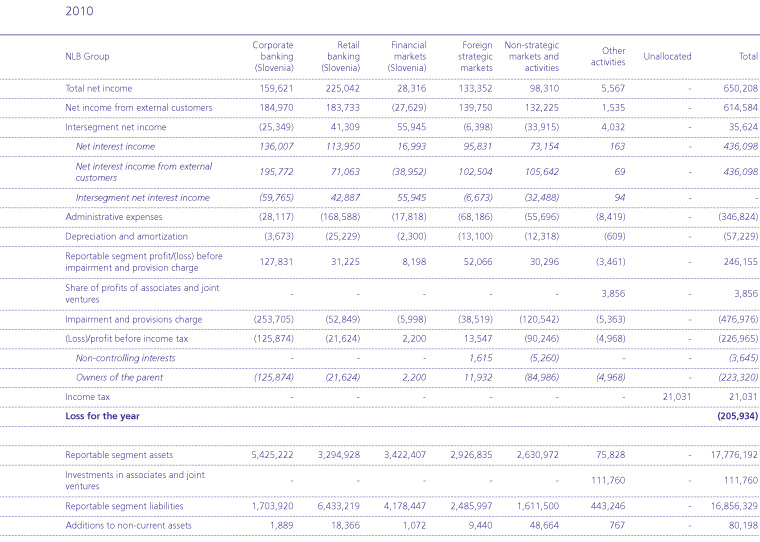

2.30. Segment reporting

Operating segments are reported in a manner consistent with internal reporting to the management board which is the executive body that makes decisions, regarding the allocation of resources and assesses the performance of a specific segment.

All transactions between business segments are conducted on a normal course of business with intrasegment income and costs eliminated. Income and expenses directly associated with each segment are included in determining segment’s performance. Income taxes are not allocated to segments (note 8.1.). The amount of net income arising from transactions between segments is disclosed in the item intersegment net income. Net income from external customers corresponds to the consolidated net income of the NLB Group.

In accordance with IFRS 8, the NLB Group has the following reportable segments: Corporate banking Slovenia, Retail banking Slovenia, Financial markets Slovenia, Foreign strategic markets, Foreign nonstrategic markets and Other activities.

In 2011 the NLB Group changed the way, how operating segments are regularly reviewed, due to a new strategy and changed internal structure of the NLB Group. Operating segments are primary split on strategic and non-strategic and further strategic on key strategic components, that are Retail banking, Corporate banking and Financial Markets.

2.31. Critical accounting estimates and judgments in applying accounting policies

The NLB Group's financial statements are influenced by accounting policies, assumptions, estimates and management judgment. The NLB Group makes estimates and assumptions that affect the reported amounts of assets and liabilities within the next financial year. All estimates and assumptions required in conformity with IFRS are best estimates undertaken in accordance with the applicable standard. Estimates and judgments are evaluated on a continuing basis, and are based on part experience and other factors, including expectations with regard to future events.

a) Impairment losses on loans and advances

The NLB Group reviews its loan portfolio to assess impairment. In determining whether an impairment loss should be recorded in the income statement, NLB Group verifies whether there are any data indicating that there is a measurable decrease in the estimated future cash flows from the portfolio of loans. This evidence may include observable data indicating that the solvency of borrowers has deteriorated or that economic conditions and circumstances have deteriorated. Future cash flows in a group of financial assets are estimated based on past experience and losses on assets with credit risk characteristics similar to those assets in the group. Individual estimates are based on projections of future cash flows taking into account all relevant information regarding the financial position and solvency of a borrower. Projected cash flows are verified by risk department. Low-value exposures, including the majority of loans to individuals, are verified collectively. The methodology and assumptions used to estimate future cash flows are reviewed regularly to reduce differences between estimated and actual losses.

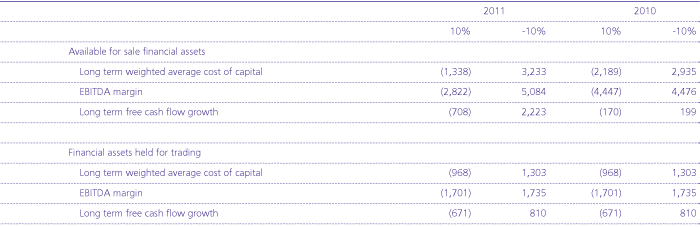

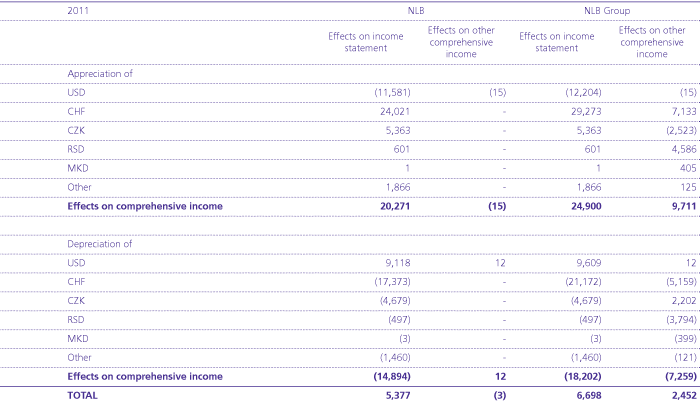

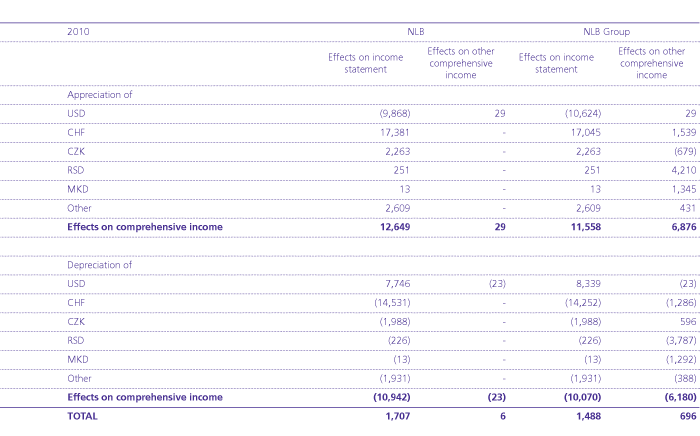

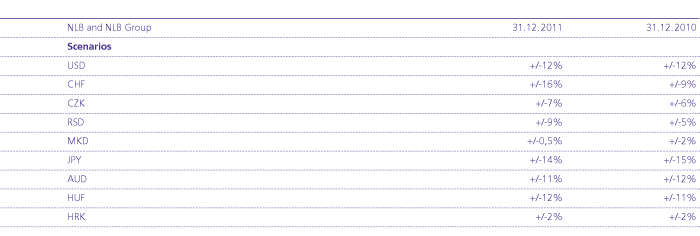

The NLB Group uses a sensitivity analysis to assess the impact of less probable negative events on impairments and provisions. Results of the simulation are based on the balance of loans and impairment as at December 31, 2011 and provide an assessment of required impairments within one year assuming the realization of the defined scenario.

Stress test using transition matrices

In the scenario historical transition matrices for financial institutions and other legal entities were used. The matrices for legal entities were also used for individuals. Exposure to the central government was not subject to the stress test. The methodology used is an extrapolation based on average transition matrices, which were calculated for the period in which the credit portfolio deteriorates. In addition, the transition matrices were corrected in a manner that excludes the possibility of client rating.

The scenario assumes that total credit exposure will not change in the one year period and the rating structure deterioration reflected through migration matrices will require additional impairments. As a result of the stress scenario, NLB will require additional impairments of EUR 261 million (2010: EUR 297 million) and the loan loss reserves to gross loan ratio will increase by 2.5 percentage points. For the NLB Group, the same stress scenario results in an increase in impairments of EUR 304 million (2010: EUR 344 million) and an increase in the coverage of the credit portfolio by impairments by 2.1 percentage points.

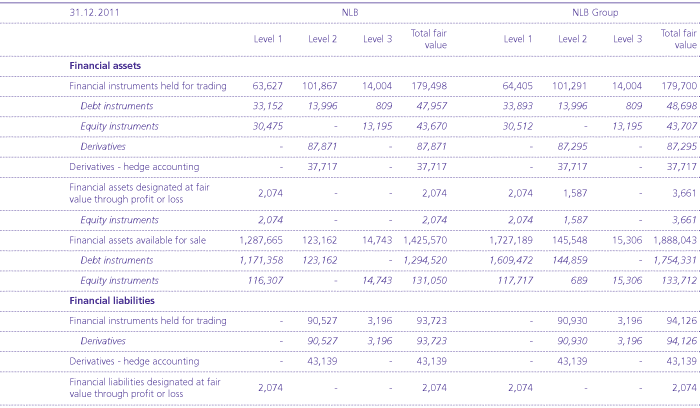

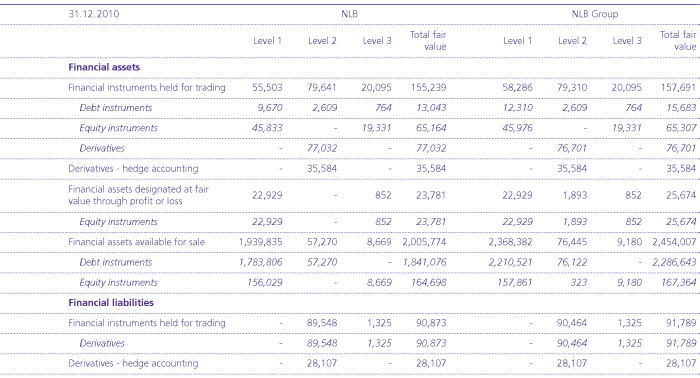

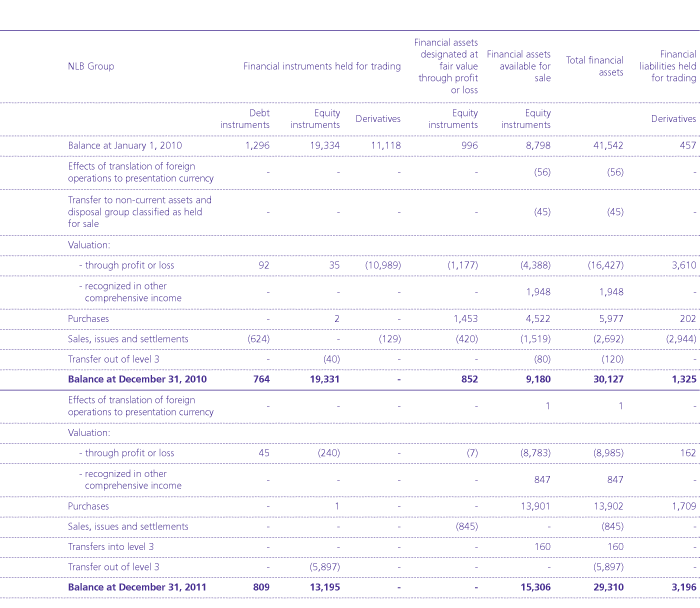

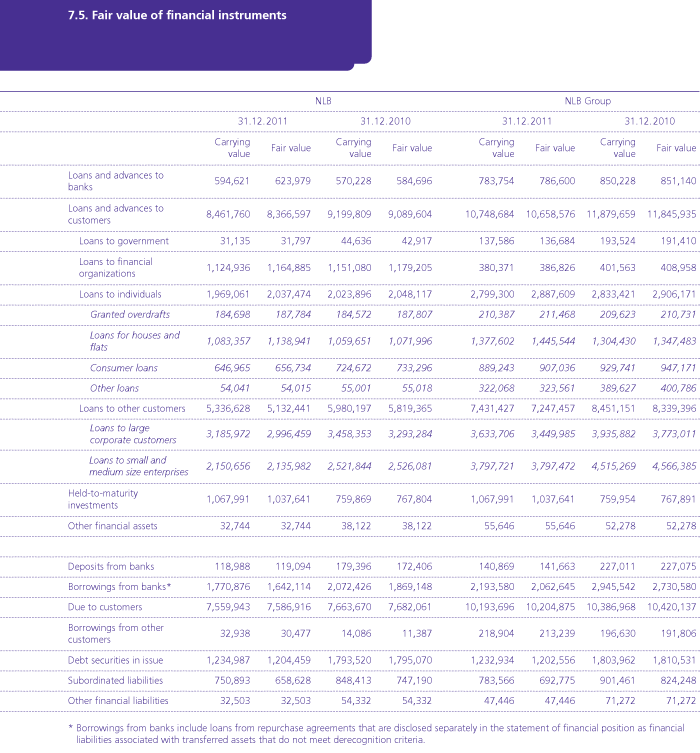

b) Fair value of financial instruments

The fair values of financial investments traded on the active market are based on current bid prices (financial assets) or offer prices (financial liabilities).

The fair values of financial instruments that are not traded on the active market are determined by using valuation models. These include a comparison with recent transaction prices, the use of a discounted cash flow model, valuation based on comparable companies and other frequently used valuation models. These valuation models pretty much reflect current market conditions at the measurement date, which may not be representative of market conditions either before or after the measurement date. Management reviewed all applied models as at the reporting date to ensure they appropriately reflect current market conditions, including the relative liquidity of the market and applied credit spread. Changes in assumptions regarding these factors could affect the reported fair values of financial instruments held for trading and available for sale financial assets.

The fair values of derivative financial instruments are determined on the basis of market data (markto- market), in accordance with the methodology for the valuation of derivative financial instruments. The market exchange rates, interest rates, yield and volatility curves used in valuation are based on the market snapshot principle. Market data is saved daily at 4 p.m. and later used for the calculation of the fair values (market value, NPV) of financial instruments. NLB applies market yield curves for valuation (see note 5.6.).

c) Available for sale equity instruments

Available for sale equity instruments are impaired, if there has been a significant or prolonged decline in fair value below historical cost. The determination of what is significant or prolonged is based on assessments. In making these assessments, the NLB Group takes into account several factors, including share price volatility. Impairment may also be indicated by evidence regarding deterioration in the financial position of the instrument issuer, deterioration in sector performance, changes in technology, and a decline in cash flows from operating and financing activities.

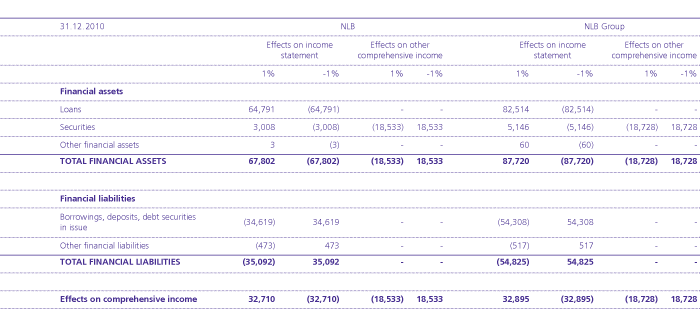

Had all the declines in fair value below cost been considered significant or prolonged, NLB would have incurred additional impairment losses of EUR 8,441 thousand (2010: EUR 44,765 thousand), while the NLB Group would have incurred additional impairment losses of EUR 9,705 thousand (2010: EUR 46,027 thousand) from the reclassification of the negative valuation from the statement of comprehensive income to the income statement for the current year.

d) Held to maturity instruments

The NLB Group classifies non-derivative financial assets with fixed or determinable payments and a fixed maturity as held to maturity investments. Before making this classification, the NLB Group assesses its intention and ability to hold such investments to maturity. If the NLB Group is unable to hold these investments until maturity, it must reclassify the entire group as available for sale financial assets. The investments would therefore be measured at fair value, resulting in a decrease in the value of investments of EUR 30,350 thousand (December 31, 2010: increase by EUR 7,937 thousand) and a corresponding other comprehensive loss.

e) Impairment of investment in subsidiaries, associates and joint ventures

The process of identifying and assessing the impairment of goodwill and other intangible assets is inherently uncertain, as the forecasting of cash flows requires the significant use of estimates, which themselves are sensitive to the assumptions used. The review of impairment represents management's best estimate of the factors such as:

- Future cash flows from individual investments depend on estimated cash flow for those periods for which formal plans are available and on assumptions regarding sustainability of and growth in cash flows in the future. The cash flows used represent management's assessment of future performance at the time of testing.

- The discount rate derived from the capital asset pricing model and used to discount future cash flows is based on the cost of equity allocated to an individual investment. The discount rate reflects the impact of range of financial and economic variables, including the risk-free rate and risk premium. The value of variables used is subject to fluctuations outside management's control.

If recoverable amount is value in use, the discounted cash flow method is used (NLB Leasing, Ljubljana, NLB Leasing Maribor, Maribor and NLB Leasing Sarajevo). When the recoverable amount is fair value less costs to sell, the value was determined based on binding offers and the estimated liquidation value (NLB Factor, Bratislava, NLB Factoring, Ostrava, NLB Serbia, Belgrade and LHB Internationale Handelsbank, Frankfurt).

If the discount rates in the discounted cash flows model differ by +/- 1 percentage point, the estimated value in use of the equity investments would be lower in case of increased discount rate by a maximum of EUR 3.5 million and in case of decreased discount rate the value in use of equity investments would be higher by a maximum of EUR 2.5 million.

If the forecasted cash flows in the discounted cash flows model differ by +/- 10 percentage point, the estimated value in use of the equity investments would be higher in case of increased forecasted cash flows by a maximum of EUR 3 million and in case of decreased forecasted cash flows the value in use of equity investments would be lower by a maximum of EUR 4.7 million.

f) Goodwill and other intangible assets

In the consolidated financial statements, goodwill and other intangible assets are allocated to cash-generating units (hereinafter: CGUs), which represent the lowest level within the NLB Group at which these assets are monitored by management. Each NLB Group entity presents a separate CGU. The recoverable amount of each CGU was determined based on value-in-use calculations. The calculation of value in use is based on cash flow projections in the three-year financial plans approved by management. The NLB Group performed a test for impairment of goodwill and other intangible assets at the end of the year for all subsidiaries.

Additional information regarding impairment testing of goodwill and other intangible assets is disclosed in note 5.13.

The goodwill for NLB Prishtina, Prishtina, represents an individually significant amount of goodwill in the NLB Group and amounts to EUR 9,738 thousand. When testing for possible impairment, the following assumptions were used: a discount rate of 13%, a growth rate for residual value of 2% p.a. and a target capital ratio of 16%. According to the test, goodwill was not impaired. If the discount rate increased for more than 7 percentage points, the carrying amount of goodwill in NLB Group would have to be impaired in amount of EUR 9,738 thousand to nil.

g) Taxes

The NLB Group operates in countries governed by different laws. The deferred tax assets recognized at December 31, 2011 are based on profit forecasts for the next five-year period and take into account expected manner of recovery of the assets, that is, whether the value will be recovered through use, sale or liquidation. Changes in the assumptions as to the likely manner of recovery of assets could lead to the recognition of currently unrecognized deferred tax assets or to derecognition of previously created deferred tax assets. In case of changed assumptions of future operations the NLB Group will adequately adjust deferred tax income assets. The NLB Group believes that this effect would be immaterial since the majority of deferred tax assets relates to tax losses which, in accordance with the Slovenian Corporate Income Tax Act, can be carried forward indefinitely.

2.32. Implementation of new and revised International Financial Reporting Standards

During the current year, the NLB Group adopted all new and revised standards and interpretations issued by the International Accounting Standards Board (hereinafter: the IASB) and the International Financial Reporting Interpretations Committee (hereinafter: the IFRIC) and endorsed by the EU that are effective for accounting periods beginning on January 1, 2011.

Accounting standards and amendments to existing standards effective for annual periods beginning on January 1, 2011 that were endorsed by EU and adopted by us

- IAS 24 (amendment) - Related Party Disclosures (effective for annual periods beginning on or after January 1, 2011). The revised standard simplifies the definition of a related party and provides a partial exemption from the disclosure requirements for government-related entities. If the exemption is applied, the entity shall disclose the nature and amount of each individually significant transaction. The amendment impacts presentation.

- Annual improvements to IFRS 2010. The improvements consist of a mixture of substantive changes and clarifications and are effective for annual periods beginning on or after January 1, 2011. IAS 27 clarifies the transition rules for amendments to IAS 21, 28 and 31 made by the revised IAS 27 (as amended in January 2008). Amendments in IAS 34 refer to interim financial reporting and affect the presentation of the NLB Group’s interim financial statement. Disclosure requirements in IFRS 7 emphasize the link between quantitative and qualitative disclosures regarding the nature and extent of financial risk and eliminates disclosures for renegotiated loans that would otherwise be past due or impaired, while disclosures regarding the fair value of collateral is replaced with a more general requirement, i.e. clarification of effect of collateral on mitigating the credit risk. Amendments to IFRS 3 require measurement of non-controlling interests at fair value, in certain cases provides guidance on an acquirer’s share-based payment arrangements that were not replaced or were voluntarily replaced as a result of a business combination, and requires that the contingent considerations from business combinations that occurred before the effective date of revised IFRS 3 are calculated using the previous IFRS 3. The amendment in IAS 1 clarifies the requirements for the presentation and content of the statement of changes in equity. Reconciliation between the carrying amount at the beginning and the end of the period for each component of equity must be presented in the statement of changes in equity, but its content is simplified by allowing an analysis of other comprehensive income by item for each component of equity to be presented in the notes. The amendments do not significantly affect the NLB Group’s financial statements.

- IFRS 7 (amendment) - Disclosures, Transfers of Financial Assets (effective for annual periods beginning on or after July 1, 2011). The amendment requires additional disclosures in respect of risk exposures arising from transferred financial assets. The amendment includes a requirement to disclose by class of asset the nature, carrying amount and a description of the risks and rewards of financial assets that have been transferred to another party yet remain on the entity's statement of financial position. Disclosures are also required to enable a user to understand the amount of any associated liabilities, and the relationship between the financial assets and associated liabilities. Where financial assets have been derecognized but the entity is still exposed to certain risks and rewards associated with the transferred asset, additional disclosure is required to enable the effects of those risks to be understood. The NLB Group is currently assessing the impact of the amended standard on disclosures in its financial statements.

- Other revised standards and interpretations effective for the current period: IFRIC 19 Extinguishing Financial Liabilities with Equity Instruments, amendments to IAS 32 Classifications of Rights of Issues, clarifications in IFRIC 14 Prepayments of a Minimum Funding Requirement and amendments in IFRS 1 Limited Exemption from Comparative IFRS 7 Disclosures for First-time Adopters did not have any impact on these financial statements.

Accounting standards and amendments to existing standards issued but not endorsed by EU:

- IFRS 9 - Financial Instruments IFRS 9 issued in November 2009 replaces those parts of IAS 39 relating to the classification and measurement of financial assets. IFRS 9 was further amended in October 2010 to address the classification and measurement of financial liabilities. Key features of the standard are as follows:

- Financial assets are required to be classified into two measurement categories: those to be measured subsequently at fair value, and those to be measured subsequently at amortized cost. The decision is to be made at initial recognition. The classification depends on the entity’s business model for managing its financial instruments and the contractual cash flow characteristics of the instrument.

- An instrument is subsequently measured at amortized cost only if it is a debt instrument and both (i) the objective of the entity’s business model is to hold the asset to collect the contractual cash flows, and (ii) the asset’s contractual cash flows represent only payments of principal and interest (i.e. it bears only “basic loan features”). All other debt instruments are to be measured at fair value through profit or loss.

- All equity instruments are to be measured subsequently at fair value. Equity instruments that are held for trading will be measured at fair value through profit or loss. For all other equity investments, an irrevocable election can be made at initial recognition, to recognize unrealized and realized fair value gains and losses through other comprehensive income rather than profit or loss. There is to be no recycling of fair value gains and losses to profit or loss. This election may be made on an instrument-by-instrument basis. Dividends are to be presented in profit or loss, as long as they represent a return on investment.

- Most of the requirements in IAS 39 for classification and measurement of financial liabilities were carried forward unchanged to IFRS 9. The key change is that an entity will be required to present the effects of changes in own credit risk of financial liabilities designated as at fair value through profit or loss in other comprehensive income.

- Adoption of IFRS 9 is mandatory from January 1, 2015, while earlier adoption is permitted, but the EU has not yet endorsed it. The NLB Group is considering the implications of the standard, the impact on the NLB Group and the timing of its adoption.

- IAS 32 (amendments) - Offsetting Financial Assets and Financial Liabilities (effective for annual periods beginning on or after January 1, 2014). The amendment added application guidance to IAS 32 to address inconsistencies identified in applying some of the offsetting criteria. This includes clarifying the meaning of ‘currently has a legally enforceable right of set-off’ and that some gross settlement systems may be considered equivalent to net settlement.

- IFRS 7 (amendments) - Offsetting Financial Assets and Financial Liabilities (effective for annual periods beginning on or after January 1, 2013). The amendment requires disclosures that will enable users of an entity’s financial statements to evaluate the effect or potential effect of netting arrangements, including rights of set-off. The amendment will have an impact on disclosures of financial instruments on the NLB Group.

- IAS 1 (amendment) - Presentation of Financial Statements (effective for annual periods beginning on or after July 1, 2012, with earlier application permitted). The amendments retain the option to present profit or loss and other comprehensive income in either a single statement or in two separate but consecutive statements. However, the amendments require additional disclosures to be made in the other comprehensive income section, such that items of other comprehensive income are grouped into two categories: items that will not be reclassified subsequently to profit or loss; and items that will be reclassified subsequently to profit or loss when specific conditions are met. Income tax on items of other comprehensive income must be allocated on the same basis. The NLB Group is currently evaluating the potential impact that the adoption of the amendments will have on the presentation of its consolidated financial statements.

- IFRS 10 - Consolidated Financial Statements, IFRS 11 - Joint Arrangements, IFRS 12 - Disclosures of Interests in Other Entities, a revised version of IAS 27 - Separate Financial Statements, which has been amended for the issuance of IFRS 10 but retains the current guidance for separate financial statements, and a revised version of IAS 28 - Investments in Associates and Joint Ventures, which has been amended for conforming changes based on the issuance of IFRS 10 and IFRS 11. Standards are effective for annual periods beginning on or after January 1, 2013, with earlier application permitted as long as each of the other standards is also applied early. However, entities are permitted to include any of the disclosure requirements in IFRS 12 into their consolidated financial statements without the early adoption of IFRS 12. The NLB Group is currently evaluating the potential impact that the adoption of the standards will have on its consolidated financial statements.

- IFRS 10 (new standard). The new standard replaces the parts of IAS 27 - Consolidated and Separate Financial Statements that deal with consolidated financial statements. SIC 12 Consolidation - Special Purpose Entities has been withdrawn upon the issuance of IFRS 10. Under IFRS 10, there is only one basis for consolidation, that being control. In addition, IFRS 10 includes a new definition of control that contains three elements: control over an investee, exposure, or rights to variable returns from its involvement with the investee, and the ability to use its control over the investee to affect the amount of the investor's returns. Extensive guidance has been added in IFRS 10 to deal with complex scenarios.

- IFRS 11 (new standard). The new standard replaces IAS 31 - Interests in Joint Ventures. IFRS 11 deals with how a joint arrangement, over which two or more parties have joint control, should be classified. SIC 13 Jointly Controlled Entities - Non-monetary Contributions by Venturers has been withdrawn upon the issuance of IFRS 11. Under IFRS 11, joint arrangements are classified as joint operations or joint ventures, depending on the rights and obligations of the parties to the arrangements. In contrast, under IAS 31, there are three types of joint arrangements: jointly controlled entities, jointly controlled assets and jointly controlled operations. In addition, joint ventures under IFRS 11 must be accounted for using the equity method of accounting, whereas jointly controlled entities under IAS 31 may be accounted for using the equity method of accounting or proportionate accounting.

- IFRS 12 (new standard). The new standard is a disclosure standard and is applicable to entities that have interests in subsidiaries, joint arrangements, associates and/or unconsolidated structured entities. In general, the disclosure requirements in IFRS 12 are more extensive than those in the current standards.

- IFRS 13 (new standard) - Fair Value Measurement (effective for annual periods beginning on or after January 1, 2013, with earlier application permitted). The standard establishes a single source of guidance for fair value measurements and disclosures about fair value measurements. The standard defines fair value, establishes a framework for measuring fair value, and requires disclosures about fair value measurements. The scope of the standard is broad; it applies to both financial instruments and non-financial instruments for which other standards require or permit fair value measurements and disclosures about fair value measurements, except in specified circumstances. In general, the disclosure requirements in IFRS 13 are more extensive than those required in the current standards. For example, quantitative and qualitative disclosures based on the three-level fair value hierarchy, currently required for financial instruments only under IFRS 7 Financial Instruments: Disclosures, will be extended by IFRS 13 to cover all assets and liabilities within its scope. The NLB Group is currently evaluating the potential impact that the adoption of the standard will have on its consolidated financial statements.

- Other revised standards and interpretations: amendments to IAS 19 - Employee Benefits, relating to the recognition and measurement of defined benefit obligations and to the disclosure to all employee benefits, amendments to IFRS 1 - Fist time Adoption of IFRS, relating to severe hyperinflation and removal of fixed dates for first-time adopters, amendment to IAS 12 - Income Taxes, relating to the recovery of underlying assets – investment property measured at fair value and amendment to IFRIC 20 - Stripping Costs in the Production Phase of a Surface Mine are not expected to affect the NLB Group’s financial statements.

3. CHANGES IN SUBSIDIARY HOLDINGS

Changes in 2011

a) Capital increase:

- The increase of share capital by cash in total amount of EUR 44,696 thousand was registered in NLB Leasing, Ljubljana, NLB Leasing, Sarajevo, Optima Leasing, Zagreb, LHB Internationale Handelsbank, Frankfurt, NLB Factoring, Ostrava, NLB Leasing Maribor, Maribor, NLB Nov penziski fond, Skopje and LHB Trade Zagreb.

- The increase of share capital by loan conversion in total amount of EUR 9,216 thousand was registered in NLB Srbija, Beograd and NLB Factor, Bratislava.

b) Other changes:

- NLB Leasing, Ljubljana sold its 100% ownership interest in NLB Leasing, Sarajevo to NLB.

- NLB Interfinanz, Zürich sold its 26.72% ownership interest in NLB Tutunska banka, Skopje to NLB.

- NLB Nova Penzija, Beograd, NLB Factor, Bratislava and NLB Tutunskabroker, Skopje were liquidated.

- NLB sold its 97.10% ownership interest in NLB Bank Sofia, Sofija (see note 5.10).

- Kreditni biro Sisbon, Ljubljana was established. The cost of establishing the company amounted to EUR 3.5 thousand. Ownership interest in Kreditni biro Sisbon, Ljubljana is 29.68%.

Changes in 2010

a) Acquisitions of additional interests in existing subsidiaries

- NLB increased its ownership interest in Plan, Banja Luka from 32.31% to 39.14%. Consideration given was EUR 90 thousand.

b) Capital increase

- The increase of share capital by cash in total amount of EUR 40,936 thousand was registered in FIN-DO, Domžale (paid in 2009), LHB Internationale Handelsbank, Frankfurt (paid in 2009), NLB Bank Sofia, Sofija, NLB banka, Beograd and NLB Leasing, Ljubljana.

- The increase of share capital by loan conversion in total amount of EUR 6,101 thousand was registered in NLB Montenegrobanka, Podgorica and NLB Srbija, Beograd.

c) Other changes

- NLB Leasing, Ljubljana sold its 100% ownership interest in NLB Leasing, Beograd to NLB.

- NLB Tuzlanska banka, Tuzla sold its 40% ownership interest in CBS Invest, Sarajevo to NLB.

- LHB Immobilien, Frankfurt sold its 60% ownership interest in CBS Invest, Sarajevo to NLB.

- NLB banka, Beograd sold its 24.61% ownership interest in Tekig Invest, Beograd.

- In May 2010 LHB Finance, Ljubljana merged with NLB.

- NLB Leasing, Ljubljana sold its 100% ownership interest in NLB Real Estate, Beograd to NLB Srbija, Beograd. In June 2010 NLB Real Estate, Beograd merged with NLB Srbija, Beograd.

4. NOTES TO THE INCOME STATEMENT

Analysis by type of assets and liabilities

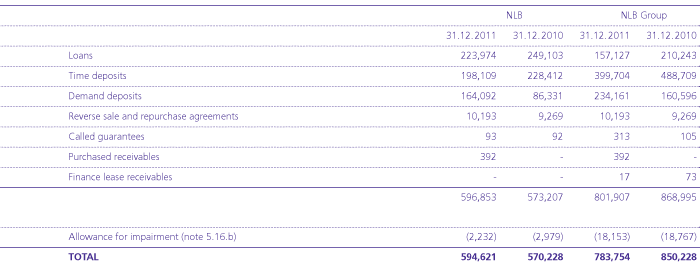

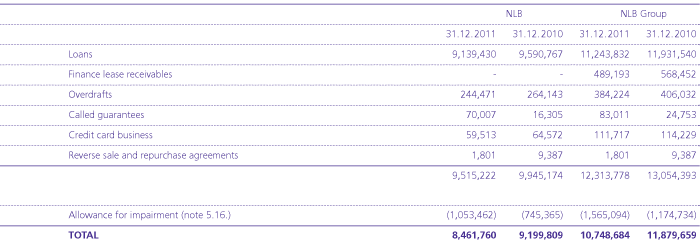

In 2011, interest income on individually impaired loans amounted to EUR 58,573 thousand for NLB (2010: EUR 33,340 thousand) and to EUR 77,600 thousand (2010: EUR 53,335 thousand) for the NLB Group.

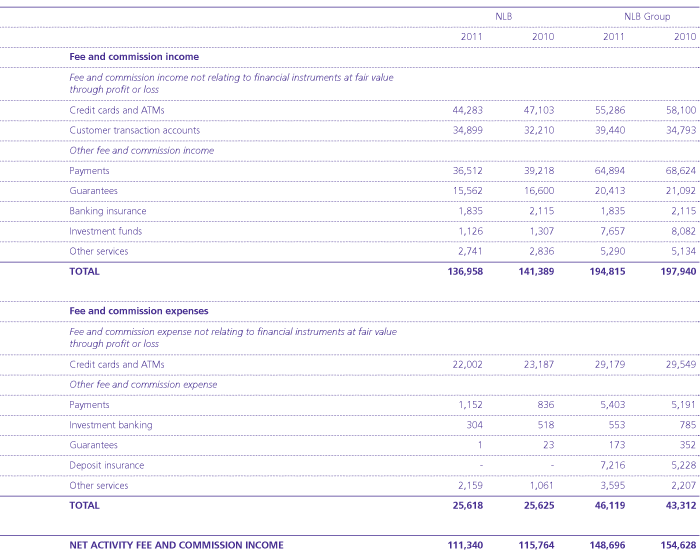

a) Fee and commission income and expenses relating to activities of NLB and the NLB Group

Other services include fees from non-banking deposit valuables and safe custody, other agency services and fees from purchase and sale of foreign exchange currencies.